Short Term Personal Loans (STPLs) are designed for immediate needs and smaller amounts, often up to ₹1 lakh. But even within this short term space, borrowers are often confused between opting for a 3-month tenure or a 6-month tenure. While both options serve different financial situations, choosing the right tenure can significantly impact your EMI amount, overall interest paid, and repayment comfort.

In this blog, we’ll break down the differences between a 3-month and 6-month STPL, evaluate their pros and cons, and help you decide which one is better suited for your current financial needs.

What Is a Short Term Personal Loan (STPL)?

A Short Term Personal Loan is an unsecured loan offered for a tenure typically ranging from 3 to 12 months. Most commonly, salaried individuals opt for 3-month or 6-month loans to meet urgent expenses like:

- Rent deposit or relocation

- Medical emergencies

- Travel costs

- Gadget or appliance purchase

- Fee payments

Since these loans are for small amounts, approvals are quick and documentation minimal—especially when done via digital aggregators like RupeeQ.

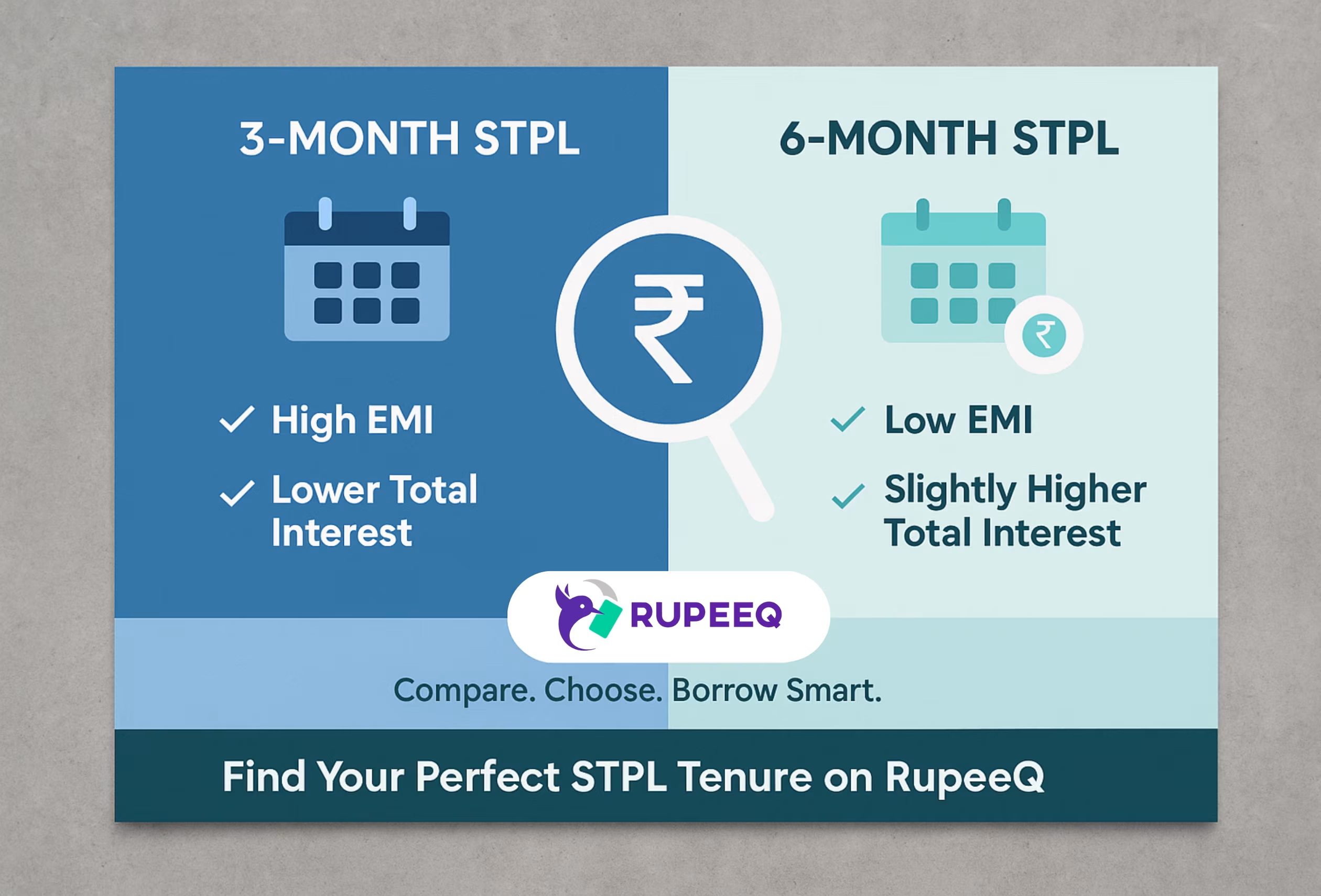

Key Differences Between 3-Month and 6-Month STPLs

Here’s a comparison table to help you quickly understand how the two tenures differ:

| Feature | 3-Month STPL | 6-Month STPL |

| Loan Tenure | 90 days | 180 days |

| EMI Amount | Higher | Lower |

| Total Interest Paid | Lower | Slightly Higher |

| Ideal For | One-time urgent needs | Mid-term budget planning |

| Monthly Budget Flexibility | Tight | More manageable |

| Approval Chance | Moderate | High (due to lower EMI risk) |

3-Month STPL: Benefits and Best Use Cases

A 3-month short term personal loan is ideal if you:

- Have a strong monthly income

- Are confident of repaying quickly

- Want to minimize interest outgo

Benefits:

- Lower Total Interest Paid:

Since the tenure is short, the lender earns interest only for three months, making it the cheaper option overall. - Faster Closure Improves Credit Score:

Clearing a loan in 3 months gives your credit score a positive push faster than a 6-month loan. - Good for One-Time Expenses:

Perfect for situations like emergency repairs, travel bookings, or paying a temporary cash gap.

RupeeQ Tip:

If you’re applying for an STPL on RupeeQ and know that your bonus or incentive is expected within 2–3 months, go for the 3-month option and close it early.

6-Month STPL: Benefits and Best Use Cases

A 6-month short term loan is preferred when:

- You want to keep EMIs smaller

- You are unsure about immediate cash inflow

- Your monthly budget is tight due to other fixed obligations

Benefits:

- Lower EMI Burden:

Spreading repayment over six months makes each EMI lighter and manageable. - Higher Approval Odds for Low Score Borrowers:

Many lenders prefer giving longer tenure loans to reduce EMI-to-income ratio. - Helps in Structuring Budget:

If your need is recurring (like tuition fees or rent deposit), the 6-month option gives better breathing room.

EMI Comparison Example

Let’s say you take a ₹30,000 STPL at 24% p.a. interest.

| Tenure | Monthly EMI (approx) | Total Interest | Total Repayment |

| 3 Months | ₹10,400 | ₹1,200 | ₹31,200 |

| 6 Months | ₹5,450 | ₹2,700 | ₹32,700 |

As seen above:

- The 3-month loan helps save ₹1,500 in interest.

- But the EMI is almost double compared to the 6-month plan.

RupeeQ Tip:

Use the RupeeQ EMI calculator before choosing tenure. Many borrowers underestimate the EMI amount for shorter durations.

How to Choose Between 3 and 6-Month STPL

Choose 3-Month STPL If:

- You have no ongoing EMIs

- You expect cash inflow (bonus, freelance income, etc.) soon

- You can manage a larger EMI without impacting your lifestyle

- You want to close the loan quickly and boost your credit score fast

Choose 6-Month STPL If:

- You are already paying home loan, vehicle loan, or other EMIs

- Your monthly savings margin is narrow

- You are unsure about job stability or income consistency

- You’re okay with paying more interest for smoother cash flow

Impact on Credit Score: Which Is Better?

Both tenures help build your credit score if paid on time. However, a 3-month loan shows quicker repayment behavior, which may reflect faster in your score improvement.

But remember—missing a single EMI in a short tenure loan has a bigger impact compared to a missed EMI in a longer loan.

So, always choose a tenure you’re confident of repaying without default.

Does Prepayment Matter in Short Term Loans?

Many lenders allow foreclosure after the first EMI. If you prepay a 6-month loan in 3–4 months, you still save on interest.

However, prepayment terms may vary:

- Some charge a flat fee

- Others may waive it after 3 EMIs

Always read the loan agreement on RupeeQ or ask the lender directly before deciding to prepay.

Final Recommendation: 3 or 6 Months?

There’s no one-size-fits-all answer. Your choice depends on:

- Cash flow clarity

- Other financial commitments

- Comfort with EMI size

- Willingness to pay higher or lower total interest

If in doubt, a 6-month STPL offers greater flexibility, while a 3-month STPL is financially cheaper.

RupeeQ Tip:

Apply via RupeeQ and filter loan offers by tenure. You’ll also get to see total repayment amount, which helps you make a more informed decision.