A personal loan can be a convenient financial solution when you need funds for medical emergencies, home renovations, weddings, education, or debt consolidation. However, taking a loan is a significant financial commitment, and applying without careful evaluation can lead to high repayment burdens or unfavorable loan terms.

Before you apply for a personal loan, it’s essential to assess key factors such as interest rates, loan tenure, eligibility, and hidden fees. Making an informed decision can help you secure the best loan offer, minimize borrowing costs, and ensure smooth repayment.

In this blog, we’ll cover the five most important factors to consider before applying for a personal loan and how RupeeQ insights can help you make the right choice.

1. Loan Amount and Purpose: Borrow Only What You Need

One of the first decisions before applying for a personal loan is determining the loan amount and its purpose. Borrowing more than necessary can lead to higher EMIs, increased interest payments, and financial strain.

Key Considerations

- Assess the exact amount needed for your expenses.

- Avoid borrowing excess funds just because you qualify for a higher loan amount.

- Have a clear repayment plan before taking a loan.

Example

Anjali needs ₹3 lakh for home renovation, but the lender offers ₹5 lakh. Taking a higher loan unnecessarily increases EMIs and total interest. Instead, she applies for the exact amount needed, ensuring manageable repayments.

2. Interest Rate: Compare and Choose the Lowest Rate

Interest rates directly impact your monthly EMI and the total cost of the loan. A lower interest rate can significantly reduce your repayment burden over the loan tenure.

Types of Personal Loan Interest Rates

- Fixed Interest Rate: The EMI remains constant throughout the tenure.

- Floating Interest Rate: EMI fluctuates based on market conditions.

Factors Affecting Interest Rates

- Credit Score: A 750+ credit score can help secure lower interest rates.

- Income Stability: Higher and stable incomes get better rates.

- Loan Amount & Tenure: Shorter tenures usually come with lower rates.

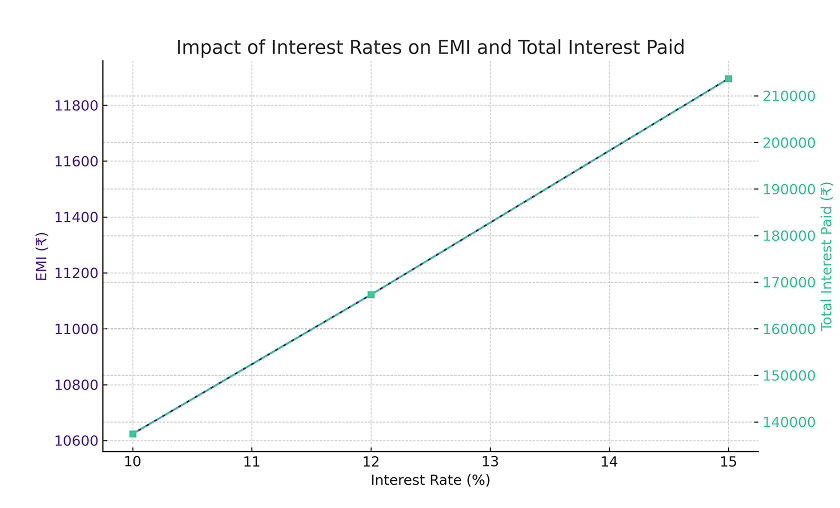

Example: Impact of Interest Rate on Loan Cost

If you take a ₹5 lakh loan for 5 years, here’s how different interest rates affect EMIs:

| Interest Rate | EMI (₹) | Total Interest Paid (₹) |

| 10% | >₹10,624 | ₹1,37,434 |

| 12% | ₹11,122 | ₹1,67,318 |

| 15% | ₹11,895 | ₹2,13,678 |

A 2% higher interest rate can increase your total repayment by ₹30,000 to ₹50,000.

RupeeQ Tip – Compare interest rates from banks, NBFCs, and digital lenders before applying. RupeeQ helps you find the lowest personal loan rates based on your credit score and income.

3. Loan Tenure: Short vs. Long-Term Loans

The loan tenure determines your EMI amount and total interest outgo.

- Shorter tenure (1-3 years): Higher EMI, but lower total interest paid.

- Longer tenure (4-7 years): Lower EMI, but higher overall interest cost.

Example: How Loan Tenure Affects EMI

For a ₹4 lakh personal loan at 12% interest, here’s the EMI difference based on tenure:

| Tenure | EMI (₹) | Total Interest Paid (₹) |

| 2 Years | ₹18,823 | ₹52,742 |

| 5 Years | ₹8,899 | ₹1,33,940 |

A longer tenure lowers EMIs but increases total interest costs, whereas a shorter tenure saves money but requires higher EMI payments.

RupeeQ Tip – Use the RupeeQ EMI Calculator to compare different tenure options and choose the one that balances affordability and cost-effectiveness.

4. Eligibility Criteria and Credit Score

Every lender has eligibility criteria based on factors such as:

- Minimum Monthly Income: ₹15,000 – ₹30,000 (varies by lender).

- Employment Type: Salaried or self-employed.

- Credit Score Requirement: Most lenders prefer 750+ scores for best loan offers.

Why Your Credit Score Matters?

A good credit score:

- Increases loan approval chances.

- Helps you get lower interest rates.

- Makes you eligible for higher loan amounts.

>Credit Score

>Approval Chances

>Interest Rate Offered>750+

>High

10-12%

| 650-749 | Moderate | 12-18% |

| Below 650 | Low | 18-24% (or rejection) |

RupeeQ Tip – Check your credit score using RupeeQ ACE before applying for a personal loan. If your score is below 700, improve it before applying to get better loan terms.

5. Hidden Fees and Charges: Know the Total Loan Cost

Apart from the interest rate, lenders charge various fees that impact the total cost of the loan.

Common Personal Loan Fees

- Processing Fees: 1-3% of the loan amount.

- Prepayment or Foreclosure Charges: 2-5% if you repay early.

- Late Payment Fees: ₹500-₹2,000 per missed EMI.

- Stamp Duty and Legal Charges: Varies by lender and state.

Example: How Fees Impact Loan Cost

If you take a ₹10 lakh loan with a 2% processing fee, you’ll pay ₹20,000 upfront, reducing your disbursed loan amount.

Final Thoughts on Making an Informed Borrowing Decision

A personal loan can provide quick financial relief, but choosing the wrong loan can lead to excessive debt and repayment difficulties. Before applying, always:

- Determine the loan amount and purpose – borrow only what you need.

- Compare interest rates – lower rates reduce your total repayment.

- Select the right loan tenure – balance affordability and cost.

- Check your credit score and eligibility – improve your score if needed.

- Be aware of hidden charges – ensure you’re not overpaying.

By carefully evaluating these factors, you can find the best personal loan deal and manage your repayments smoothly.

Looking for a personal loan with the lowest fees and best interest rates? Compare offers on RupeeQ today!