A personal loan comes with a fixed repayment schedule, typically spanning 1 to 7 years. However, if you find yourself in a position to repay the loan early, you might wonder: Can I prepay my personal loan? And should I?

The answer is yes, you can prepay a personal loan, but it’s important to understand the costs, benefits, and conditions associated with prepayment before making a decision. While prepaying a loan can help you save on interest, some lenders offer loan prepayment guide that may offset the savings.

In this blog, we’ll cover:

- What is personal loan prepayment?

- Types of prepayment (part-payment vs. foreclosure)

- Benefits and drawbacks of prepaying a loan

- How to calculate savings from prepayment

- RupeeQ insights on when prepayment makes sense

What is Personal Loan Prepayment?

Personal loan prepayment refers to repaying the loan amount before the scheduled tenure ends. Borrowers can choose to either:

✔ Part-prepay – Pay a lump sum amount before the full tenure, reducing the principal and future EMIs.

✔ Foreclose the loan – Repay the entire outstanding balance in one go and close the loan early.

Different lenders have varied prepayment rules. Some allow prepayment after 6 or 12 months, while others impose penalties on early closure.

2. Types of Prepayment: Part-Prepayment vs. Foreclosure

| Prepayment Type | How It Works | Benefit | Drawback |

| Part-Prepayment | Paying a lump sum amount but continuing EMIs | Reduces loan principal and interest | Some lenders charge fees |

| Foreclosure | Paying off the entire loan early | No more EMIs, saves total interest | Foreclosure fees may apply |

Example: Impact of Prepayment on Loan Repayment

Let’s say you have a ₹5 lakh personal loan at 12% interest for 5 years (60 months).

| Scenario | EMI (₹) | Total Interest Paid (₹) | Total Loan Cost (₹) |

| Regular Repayment | ₹11,122 | ₹1,67,318 | ₹6,67,318 |

| Part-Prepayment After 2 Years (₹1.5L) | ₹11,122 (reduced tenure) | ₹1,29,540 | ₹6,29,540 |

| Foreclosure After 2 Years | ₹0 | ₹97,000 (interest paid) | ₹5,97,000 |

If you foreclose after 2 years, you save approximately ₹70,000 – ₹1 lakh in interest payments!

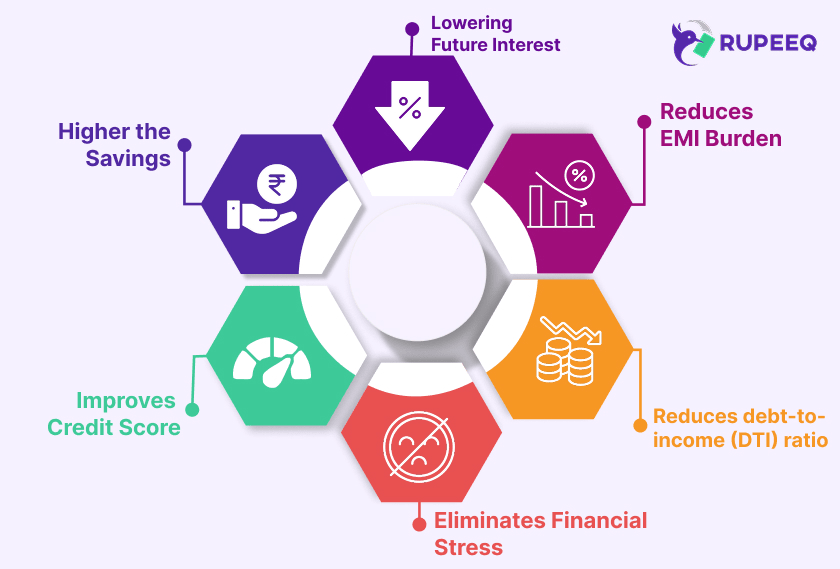

Benefits of Prepaying a Personal Loan

Saves Money on Interest

- Prepaying reduces the remaining loan principal, thereby lowering future interest payments.

- The earlier you prepay, the higher the savings.

Reduces EMI Burden

- Some lenders allow EMI reduction instead of tenure reduction, making repayments easier.

Eliminates Financial Stress

- Loan closure reduces monthly liabilities, improving cash flow for other financial goals.

Improves Credit Score

- Successfully repaying a loan early enhances creditworthiness.

- Reduces debt-to-income (DTI) ratio, increasing eligibility for future loans.

Drawbacks of Prepaying a Personal Loan

Prepayment Charges Can Offset Savings

- Lenders often charge 2% – 5% of the outstanding loan amount as a prepayment penalty.

Loss of Tax Benefits (If Applicable)

- If the loan was taken for business purposes or specific tax-saving schemes, prepayment may reduce tax deductions.

Liquidity Constraints

- Using savings for prepayment can leave you without emergency funds.

- If you have low-interest debts, it might be better to invest instead.

RupeeQ Tip – Before prepaying, check if the interest savings exceed the prepayment penalty. If the penalty is too high, invest surplus funds instead of prepaying.

How to Calculate Prepayment Savings?

Let’s assume you have a ₹7 lakh loan at 14% for 5 years.

| Scenario | EMI (₹) | Total Interest Paid (₹) | Prepayment Charges (₹) | Total Savings (₹) |

| No Prepayment | ₹16,307 | ₹2,79,835 | ₹0 | ₹0 |

| Part-Prepayment After 2 Years (₹2L) | ₹16,307 | ₹1,94,350 | ₹5,000 | ₹80,000+ |

| Foreclosure After 2 Years | ₹0 | ₹1,54,000 | ₹10,000 | ₹1,00,000+ |

✔ If prepayment savings exceed the penalty, go ahead.

✔ If the penalty is high, invest instead.

When Should You Prepay Your Loan?

If You Have a High-Interest Loan

- If your loan interest rate is above 14%, prepayment saves substantial interest costs.

If You Have Surplus Savings

- If you have excess funds, prepaying a loan reduces financial stress.

If Your Credit Score Needs Improvement

- Closing a loan early lowers your debt-to-income ratio, improving future loan eligibility.

When NOT to Prepay a Loan?

- If the prepayment penalty is too high (above 3%).

- If you lack emergency savings—don’t use all your cash reserves.

- If your personal loan interest rate is below 10%, it may be better to invest the surplus funds.

RupeeQ Tip – Compare prepayment charges across lenders before taking a loan. Some banks offer zero prepayment charges for salaried individuals.

How to Prepay a Personal Loan? (Step-by-Step Guide)

Step 1: Contact Your Lender

- Ask about outstanding balance, prepayment charges, and loan closure procedure.

Step 2: Submit Prepayment Request

- Visit the bank or apply online (if your lender allows digital prepayment).

- Provide loan account number, ID proof, and bank details.

Step 3: Make the Payment

- Use NEFT, RTGS, or cheque payment to clear the outstanding balance.

Step 4: Collect Loan Closure Certificate

- Ensure you receive a Loan Closure Statement (NOC) as proof of full repayment.

Is Prepayment Right for You?

Prepay your personal loan if:

- You want to reduce total interest costs.

- You have surplus savings and don’t need liquidity.

- The prepayment charges are minimal or zero.

Avoid prepayment if:

- Your interest rate is low (below 10%) and investing makes more sense.

- You don’t have sufficient emergency funds.

- The prepayment penalty cancels out the interest savings.

By understanding your loan terms and financial goals, you can make a smarter decision about personal loan prepayment.

Want to check prepayment charges or compare loan options? Use RupeeQ Loan Comparison Tool today! 🚀