Short Term Personal Loans (STPLs) are gaining popularity among salaried individuals and gig workers in India. These loans are often small-ticket, quick-disbursal products designed to meet urgent cash needs—ranging from ₹10,000 to ₹1,00,000. But before hitting that ‘Apply’ button on RupeeQ, most users have a list of doubts and clarifications.

In this blog, we answer the most commonly asked questions RupeeQ users raise before applying for an STPL. Whether you’re applying for the first time or comparing lenders, this blog will help you make an informed decision.

1. What is the typical loan amount for a short term personal loan?

STPLs are meant for immediate, smaller financial needs. Most RupeeQ users apply for loans ranging from ₹10,000 to ₹1 lakh. The actual amount you can get depends on your monthly income, credit profile, and repayment capacity.

Typical Use-Cases Include:

- Paying rent or security deposit

- Managing medical expenses

- Purchasing electronic gadgets

- Meeting travel expenses

- Handling education-related shortfalls

RupeeQ Tip:

If you are unsure of how much you’re eligible for, check your pre-approved limit on RupeeQ using just your PAN and mobile number.

2. Who is eligible for a short term personal loan?

Eligibility criteria vary from lender to lender, but on RupeeQ, most STPLs require:

- Age: 21 to 58 years

- Minimum monthly salary: ₹15,000 – ₹20,000

- Employment: Salaried or self-employed with proof of income

- Bank account with salary/income credit

- A minimum credit score (usually 600+)

Even if your credit score is on the lower side, you may still get offers on RupeeQ from lenders open to new-to-credit or low-score borrowers.

3. How quickly is the loan disbursed?

This is one of the biggest USPs of STPLs. Once your application is submitted and approved, disbursal is usually done within a few hours to 24 hours.

Some lenders integrated with RupeeQ offer:

- eKYC-based instant approvals

- Auto-verified salary slips via bank statements

- Direct credit to your bank account the same day

However, delays can happen if documents are incomplete or if manual verification is needed.

4. What are the interest rates for STPLs?

Interest rates for STPLs are usually higher than long-term loans due to their short tenure and unsecured nature. The rates on RupeeQ typically range from:

- 18% to 36% p.a., depending on your profile and the lender

While this may look high annually, remember that STPLs are taken for 3 to 12 months, so the absolute interest amount is usually low.

Example:

A ₹20,000 loan at 24% p.a. for 3 months may cost only around ₹1,000 in interest.

5. What documents are required?

Most STPLs today are completely paperless, especially when applied online through RupeeQ. You will usually need:

- PAN Card

- Aadhaar Card

- Bank statement (last 3–6 months)

- Salary slip (last 1–2 months) or Form 16

Some lenders might ask for additional documents like address proof or employment letter, especially if your credit score is borderline.

6. What are the repayment options?

STPLs are repaid via monthly EMIs. These are automatically deducted via NACH (National Automated Clearing House) mandate linked to your bank account.

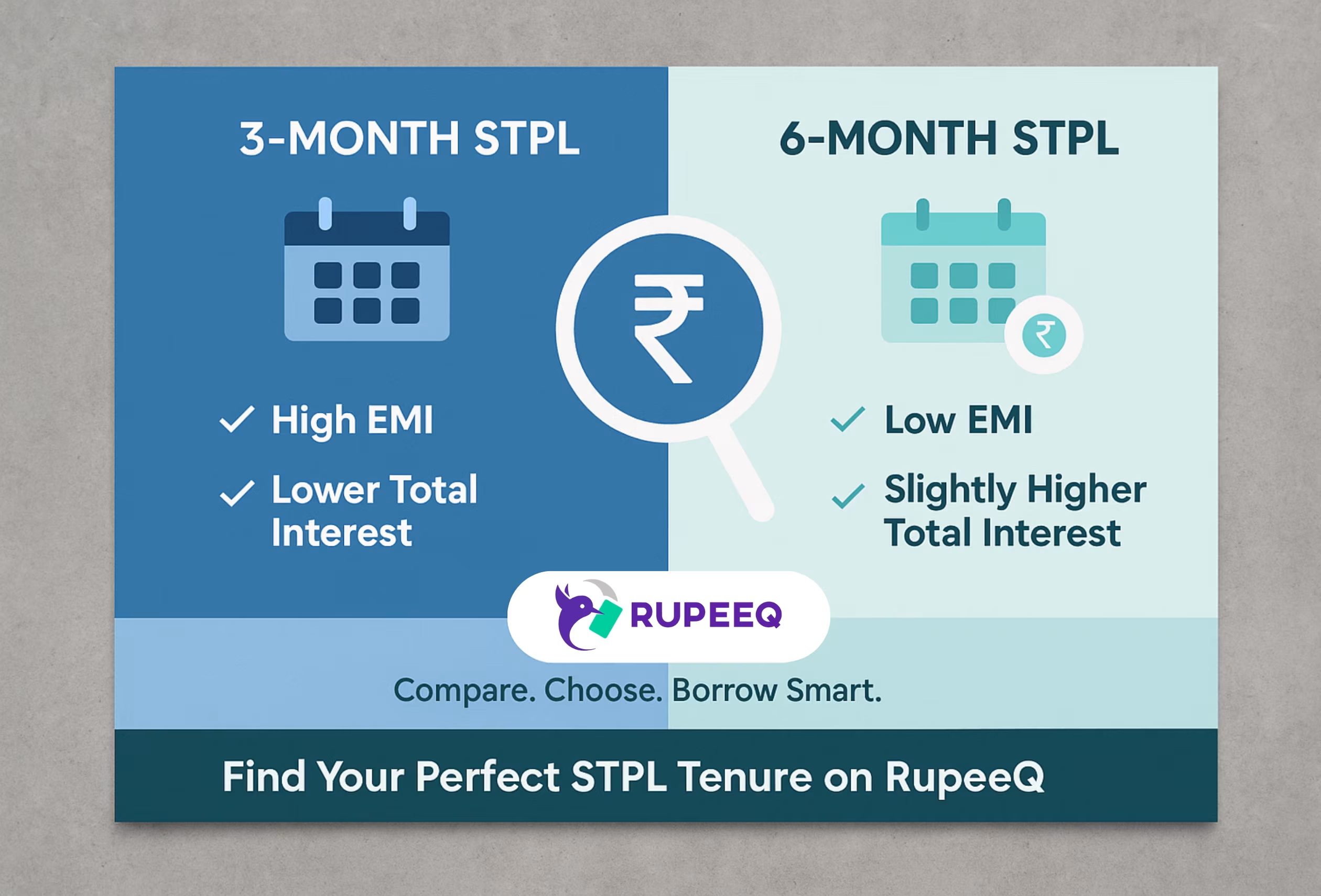

Tenure Options on RupeeQ:

- 3-month

- 6-month

- 9-month

- 12-month

Shorter tenure = higher EMI, lower total interest

Longer tenure = lower EMI, higher total interest

RupeeQ Tip:

Use the EMI calculator on RupeeQ before selecting a tenure. This helps you compare offers and understand your monthly outflow better.

7. Can I repay the loan before tenure?

Yes, most STPL lenders allow prepayment or foreclosure after a certain number of EMIs. Some may charge a nominal penalty (1%–3%), while others may allow it for free after 3 EMIs.

Always check:

- Lock-in period

- Foreclosure fee

- Process (online/offline)

Prepaying early saves you money on interest, especially for 6 to 12-month loans.

Before applying for an STPL, be sure to review the following:

Charge Type |

Typical Range |

Processing Fee |

1% – 3% of loan amt |

Late Payment Fee |

₹200 – ₹500 per EMI |

Foreclosure Charges |

0% – 4% |

NACH Bounce Penalty |

₹250 – ₹750 |

GST on Charges |

18% |

Always read the loan agreement carefully before accepting any offer.

9. Will applying for STPL affect my credit score?

Yes, it can—but how it affects your score depends on repayment behavior.

- Timely repayments boost your credit score

- Multiple loan applications in a short time can slightly reduce score temporarily

- A missed EMI can bring down your score significantly

RupeeQ Tip:

Avoid applying with too many lenders at once. RupeeQ filters offers and lets you apply with lenders most likely to approve you, thus protecting your credit score from unnecessary inquiries.

10. Can I apply again after repaying one STPL?

Absolutely. In fact, lenders are more likely to offer better terms (higher loan amount, lower interest rate) if you’ve successfully repaid a previous STPL on time.

Some users who took ₹30,000 in their first loan may be eligible for ₹50,000–₹1 lakh in their next loan cycle via RupeeQ.

11. Are there STPL options for low credit score users?

Yes. RupeeQ partners with lenders who are open to:

- New-to-credit users

- Users with scores as low as 580

- Borrowers with minor EMI delays in the past

That said, interest rates and approval amounts may be more conservative. Focus on repaying your STPL responsibly to improve future eligibility.

Conclusion

Short Term Personal Loans are a powerful financial tool—if used correctly. As RupeeQ users explore their first or next STPL, it’s natural to have questions. Hopefully, this guide helped answer the most frequent concerns and gave you clarity on what to expect.

Want to know your eligibility in 60 seconds?

Check your offers on RupeeQ with zero paperwork and no credit score impact.