When applying for a short term personal loan, one of the most important things to evaluate is the interest rate offered by lenders. It directly affects your monthly EMI and the total cost of borrowing. While these loans are quick and easy to access, interest rates can vary significantly depending on a variety of factors.

In this article, we break down the key elements that influence the interest rate on a short term personal loan (STPL) so you can borrow smarter and manage your finances more effectively.

What Is a Short Term Personal Loan and Why Interest Rate Matters

Short term personal loans are small-ticket, unsecured loans typically ranging between ₹10,000 and ₹1 lakh, with tenures between 3 and 12 months. These loans are commonly used to fund urgent lifestyle needs, travel, tuition, gadgets, or medical expenses.

The interest rate you are offered determines:

- The monthly EMI

- The total repayment amount

- Your loan affordability

Even a small difference in rate—say 18% vs. 22%—can have a significant impact on your repayment.

1. Your Credit Score

Your credit score is often the most influential factor in determining the interest rate on your loan. A high credit score reflects financial discipline and lower risk for the lender, leading to better loan terms.

| Credit Score Range | Typical Interest Rate (p.a.) |

| 750 and above | 12% to 16% |

| 700 – 749 | 17% to 20% |

| Below 700 | 21% and above |

RupeeQ Tip:

Before applying, check credit score for free on RupeeQ. This helps you compare offers suited to your profile.

2. Loan Amount and Tenure

The amount you borrow and the repayment tenure selected also influence your interest rate.

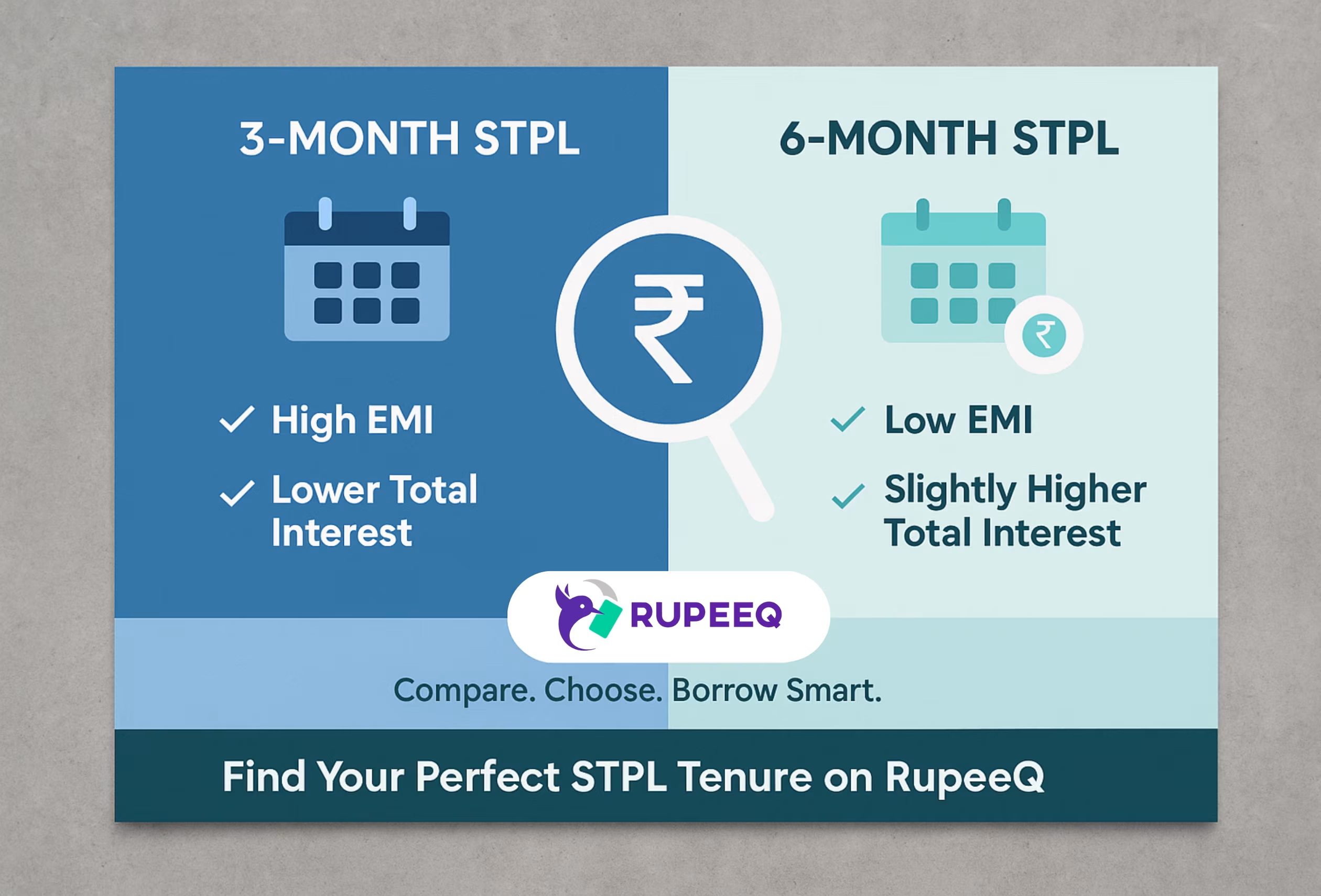

- Lower amounts like ₹10,000 to ₹30,000 may attract higher interest rates due to administrative cost coverage.

- Very short tenures (like 3 months) may result in higher rates as lenders recover cost over a shorter period.

- A slightly longer tenure (6 to 9 months) often comes with a marginally reduced rate.

Example:

A ₹30,000 loan for 3 months might have a 22% p.a. rate, while the same loan for 6 months could be available at 18% p.a.

3. Income and Employment Type

Lenders assess your monthly income and employment type to understand your repayment capacity.

- Salaried professionals with a stable monthly income are seen as low-risk and often receive better rates.

- Self-employed individuals or freelancers may face slightly higher rates due to variable income patterns.

- Holding a job in a reputed company or working in a government role also helps fetch a better rate.

4. Debt-to-Income Ratio

Even if your salary is high, lenders look at how much of it is already committed to existing EMIs. This is known as your Debt-to-Income (DTI) ratio.

- Ideally, your DTI should be below 40%

- Higher DTI ratios lead to higher perceived risk and therefore higher interest rates

Calculation Example:

If you earn ₹40,000 per month and already pay ₹18,000 in EMIs, your DTI is 45%. This might negatively affect your loan rate.

5. Loan Purpose and Profile Match

The stated purpose of your loan may also influence the rate. For example:

- Loans for education, career growth, or medical emergencies often get better rates

- Loans for shopping or gadgets may be seen as discretionary and priced slightly higher

Lenders also check if your profile aligns with typical users for a given loan type. Platforms like RupeeQ use advanced profile matching to suggest the best-suited offers.

6. Existing Relationship with the Lender

If you already have a salary account, fixed deposit, or previous loan with a bank or NBFC, you may qualify for preferential rates.

Existing customers are considered lower risk as the lender has more insight into your financial behavior.

RupeeQ Tip:

Filter lenders on RupeeQ by relationship status to check if you’re eligible for any special rate or pre-approved offer.

7. Lender Type and Pricing Model

Different types of lenders apply different pricing strategies.

- NBFCs and Digital Lenders: Often quick with approval and flexible with documentation but may charge slightly higher rates (18%–28%).

- Banks: Offer lower rates (11%–18%) but may have stricter eligibility criteria.

- Fintech Platforms: Aggregate offers and show you multiple options in one go.

Comparing across lender types can save you thousands in interest.

8. Promotional Offers or Limited-Time Discounts

Some lenders periodically run limited-time offers where they reduce interest rates for certain segments or campaigns—especially during festivals, end-of-season sales, or co-branded tie-ups.

Always check if you can benefit from one of these campaigns while applying.

9. Co-applicant or Guarantor Presence

In rare cases, having a co-applicant or guarantor can help reduce the interest rate, particularly if the co-applicant has a strong credit profile. This is more common for higher-ticket loans but can sometimes help with STPLs too.

10. Risk Category Defined by the Lender

Lenders use proprietary risk scoring systems to assess borrower profiles. Based on this, you may be classified into one of the following internal tiers:

- Prime – lowest rate

- Near-prime – mid-range rate

- Sub-prime – higher rate

These internal categories vary from one lender to another, but credit score, income, and stability form the basis.

Sample EMI Comparison Table by Rate

| Loan Amount | Tenure | Interest Rate | EMI/month |

| ₹30,000 | 6 month | 16% | ₹5,323 |

| ₹30,000 | 6 month | 22% | ₹5,486 |

| ₹50,000 | 9 month | 14% | ₹6,052 |

| ₹50,000 | 9 month | 20% | ₹6,327 |

As seen above, a small difference in interest rate can lead to significantly higher repayments.

Summary: Borrow Smart, Compare Wisely

Interest rates on short term personal loans are influenced by multiple factors—some within your control (credit score, income) and some dependent on lender strategy. Being aware of these allows you to time your application better and compare offers with greater confidence.

Key takeaway:

Always compare loan offers on trusted platforms like RupeeQ, understand total cost of borrowing, and choose a tenure that balances EMI affordability with lower interest outgo.