If you’ve ever struggled with juggling multiple EMIs, you’ve likely heard of debt consolidation. But what if you’ve already done it once? Can you do it again? And if so, how many times? These are common and valid concerns—especially for salaried borrowers or self-employed individuals trying to simplify their finances.

In this blog, we’ll explore how many times you can consolidate a loan, the conditions that apply, and how to use this strategy wisely without risking your credit health.

What Is Loan Consolidation?

Loan consolidation involves combining multiple existing debts—like personal loans, credit card dues, or consumer finance EMIs—into one single loan. This is done to:

- Reduce the number of EMIs

- Lower the overall interest rate

- Improve repayment convenience

This method helps simplify your financial life, especially if you’re dealing with too many due dates and interest rates at once.

Is There a Limit to How Many Times You Can Consolidate a Loan?

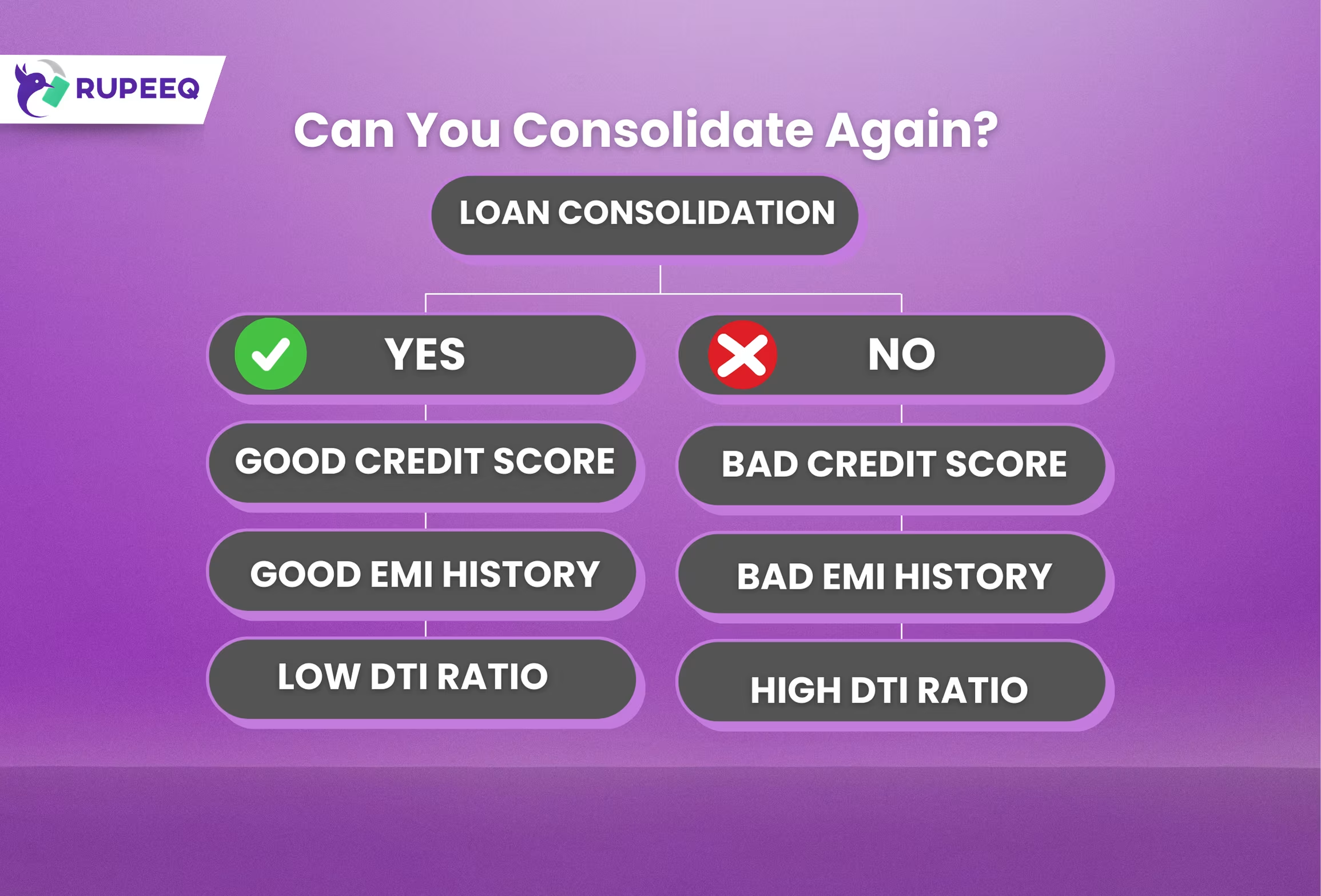

Technically, there’s no fixed legal or regulatory limit to how many times you can consolidate a loan in India. As long as you meet the lender’s eligibility criteria, you can opt for consolidation multiple times.

However, there are certain factors that determine whether repeated consolidations are possible:

Key Factors That Affect Repeated Loan Consolidation

Let’s break down the conditions that affect your ability to consolidate loans more than once:

1. Credit Score and History

Every loan you take—whether for consolidation or not—affects your credit report. If you’ve recently consolidated and missed EMIs or closed loans too early, your score might drop, making it harder to get another consolidation loan.

RupeeQ Tip: Always check your free credit score on RupeeQ before applying again. A score above 720 improves your chances.

2. Debt-to-Income (DTI) Ratio

DTI measures how much of your monthly income goes toward debt repayments. If this number is too high (typically over 40–50%), lenders may reject your new consolidation request.

Example:

- Monthly income = ₹60,000

- Total EMI burden = ₹30,000

- DTI = 50% (very risky for lenders)

3. Recent Loan Enquiries

If you’ve applied for multiple loans or credit cards recently, your credit report will show several hard inquiries. Too many hard inquiries in a short span can reduce approval chances for another consolidation loan.

4. Existing Loan Performance

If you consolidated your debt once and are repaying it without delays, lenders may see you as reliable. But if you missed payments, defaulted, or opted for settlements, your eligibility for future consolidation loans may drop.

5. Lender’s Internal Policy

Some lenders restrict the number of personal or consolidation loans within a certain time period (e.g., one loan every 6–12 months). Always check specific lender policies when applying again.

When Does It Make Sense to Consolidate Again?

Here are 3 real-life situations where it may be practical to consolidate more than once:

Scenario 1: You Took a Short-Term Consolidation Loan Initially

If your first consolidation loan was for a short tenure (say 6–12 months), you may need another round of consolidation after clearing or nearing the end of that loan.

Scenario 2: New High-Interest Loans Have Been Added

If you’ve taken new high-interest credit (e.g., BNPL, credit card EMIs) after your first consolidation, you may choose to consolidate again for interest savings.

Scenario 3: Your Credit Score Has Improved

With a better credit score, you might get access to better terms, allowing you to refinance or consolidate again at a lower interest rate.

How Many Times Is Too Many?

While there’s no numeric limit, repeated consolidations within short intervals can be seen as a sign of financial instability. This may:

- Reduce your creditworthiness

- Lower chances of loan approvals in future

- Increase your dependence on debt

As a thumb rule, avoid consolidating more than once every 12–18 months unless absolutely necessary.

Table: When to Consider Consolidation Again

| Situation | Should You Consolidate Again? | Why? |

| Cleared first loan & new high-interest debt added | ✅ Yes | Reduces cost & simplifies EMIs |

| Still repaying first consolidation loan | ❌ No | Better to finish current one |

| Credit score has improved >750 | ✅ Yes | May get better rate/tenure |

| Too many new loans recently | ❌ No | Reflects poor credit behavior |

| Facing job/income instability | ❌ No | May increase financial stress |

How to Apply for Debt Consolidation Again

- Check Credit Score: Use RupeeQ’s free credit score feature to know your latest score.

- Compare Consolidation Offers: Find the best offer as per your running loans.

- Use EMI Calculator: Compare current EMIs vs. consolidated loan offer.

- Apply Smartly: Choose the best lender offering low interest and flexible tenure.

RupeeQ Tip: Before going for another round of consolidation, try improving your credit health by reducing your credit card usage or clearing smaller loans manually. This will help you get better loan offers if you choose to consolidate again.

Final Thoughts

You can consolidate your loan multiple times—but that doesn’t mean you always should. Lenders allow it, but your credit score, EMI burden, and financial stability play a big role. Use this tool wisely and not as a recurring escape from poor repayment discipline.

If you’re ready to simplify your EMIs again, use RupeeQ to explore the best consolidation loan offers tailored to your profile.