When faced with an urgent financial need, two common borrowing options are credit cards and personal loans. Both allow access to funds without requiring collateral, but they serve different financial needs and come with distinct repayment structures.

A credit card is best for short-term, smaller expenses, offering a revolving credit limit and benefits like reward points and cashback. A personal loan, on the other hand, is more suitable for larger, planned expenses, with structured EMIs (Equated Monthly Installments) and lower interest rates.

Choosing the right option depends on your financial needs, repayment ability, and cost considerations. In this blog, we’ll compare credit cards and personal loans based on key factors like interest rates, repayment flexibility, borrowing limits, and hidden charges, so you can make an informed decision.

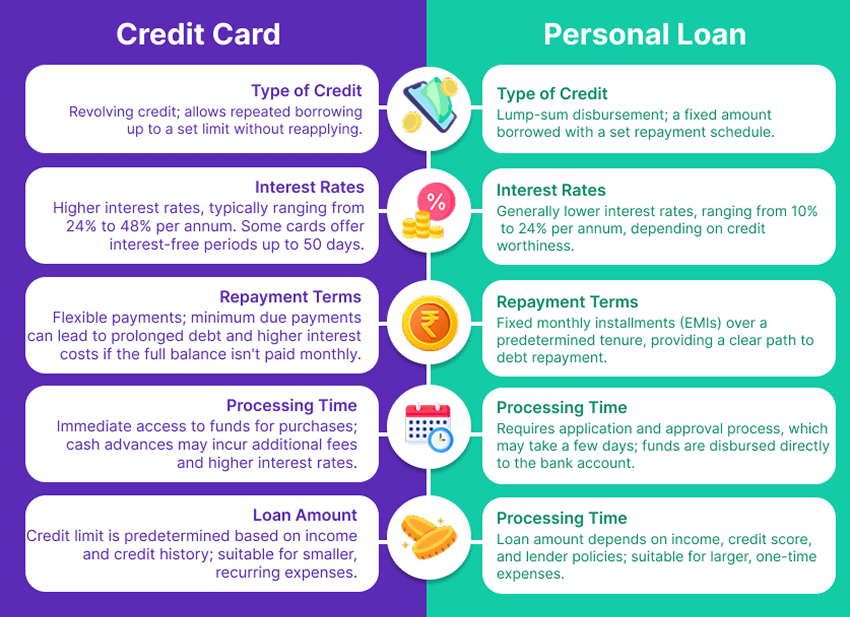

Key Differences Between Credit Cards and Personal Loans

| Feature | Credit Card | Personal Loan |

| Type of Credit | Revolving credit; allows repeated borrowing up to a set limit without reapplying. | Lump-sum disbursement; a fixed amount borrowed with a set repayment schedule. |

| Interest Rates | Higher interest rates, typically ranging from 24% to 48% per annum. Some cards offer interest-free periods up to 50 days. | Generally lower interest rates, ranging from 10% to 24% per annum, depending on creditworthiness. |

| Repayment Terms | Flexible payments; minimum due payments can lead to prolonged debt and higher interest costs if the full balance isn’t paid monthly. | Fixed monthly installments (EMIs) over a predetermined tenure, providing a clear path to debt repayment. |

| Loan Amount | Credit limit is predetermined based on income and credit history; suitable for smaller, recurring expenses. | Loan amount depends on income, credit score, and lender policies; suitable for larger, one-time expenses. |

| Processing Time | Immediate access to funds for purchases; cash advances may incur additional fees and higher interest rates. | Requires application and approval process, which may take a few days; funds are disbursed directly to the bank account. |

| Documentation | Minimal documentation required; existing credit cardholders can access funds quickly. | Requires submission of income proof, identity, and address verification; more extensive documentation compared to credit cards. |

| Collateral | Unsecured; no collateral required. | Unsecured; no collateral required. |

RupeeQ Tip – If you need flexibility and frequent access to credit, a credit card is ideal. If you need a one-time lump sum for a planned expense, a personal loan is better due to lower interest rates and structured repayment.

When to Choose a Credit Card

- Short-Term, Smaller Expenses: Ideal for everyday purchases like groceries, dining, or minor emergencies that can be paid off within the interest-free period.

- Rewards and Benefits: Beneficial if you can take advantage of cashback, reward points, or travel miles by paying off the balance monthly to avoid interest charges.

- Building Credit History: Regular, responsible use can help establish or improve your credit score.

Caution: Carrying a balance beyond the interest-free period can lead to high-interest charges. It’s essential to monitor spending to prevent debt accumulation.

When to Choose a Personal Loan

- Large, One-Time Expenses: Suitable for significant expenditures such as home renovations, weddings, medical emergencies, or debt consolidation.

- Structured Repayment Plan: Fixed EMIs over a set tenure provide predictability in budgeting and a clear timeline for debt repayment.

- Lower Interest Rates: Generally more cost-effective for borrowing larger amounts compared to carrying a balance on a credit card.

Caution: Ensure you can commit to the fixed repayment schedule to avoid penalties or negative impacts on your credit score.

Interest Rate Comparison: Which is More Affordable?

Interest rates play a crucial role in deciding between a credit card and a personal loan.

- Credit Card Interest Rates: 24% – 48% p.a. (if balance is not repaid within the due date).

- Personal Loan Interest Rates: 10% – 24% p.a. (depends on credit score and income).

When to Choose a Credit Card?

- If you can pay the full balance before the due date to avoid interest.

- For short-term expenses like dining, shopping, or travel bookings.

When to Choose a Personal Loan?

- If you need a large amount (₹1 lakh – ₹50 lakh).

- If you require a structured repayment plan with fixed EMIs.

RupeeQ Tip – If you cannot repay the credit card balance in full, opt for a personal loan instead to avoid excessive interest charges.

Loan Amount and Borrowing Limits

| Factor | Credit Card | Personal Loan |

| Loan Limit | Pre-approved limit based on income and credit score | Higher loan amount based on eligibility |

| Best for | Smaller, frequent expenses | Large, planned expenses |

| Approval Time | Instant for transactions | Requires application, typically 24 – 48 hours |

Example

Rahul has a credit card limit of ₹1.5 lakh, but he needs ₹5 lakh for a home renovation. In this case, a personal loan is a better choice since a credit card won’t cover the full cost and would lead to high interest if used.

When to Choose What?

- Use a credit card for expenses up to ₹1 lakh that can be repaid quickly.

- Use a personal loan for expenses over ₹1 lakh, which require structured repayment.

Final Thoughts: Which One Should You Choose?

Choose a Credit Card If:

- You need short-term credit and can pay off the bill in full each month.

- You want reward points, cashback, and discounts.

- You prefer a flexible spending limit without long-term commitments.

Choose a Personal Loan If:

- You need a large amount for planned expenses like home renovation or weddings.

- You want structured repayment with fixed EMIs.

- You are looking for lower interest rates compared to credit cards.