Managing a total debt of ₹10 lakh may seem daunting, especially when it’s spread across different EMI-based loans. But with the right strategy and financial discipline, clearing it is entirely achievable. Whether your debt is the result of multiple personal loans, BNPL services, or home renovation loans, you can pay it off systematically—without stress or confusion.

This blog outlines a clear, step-by-step repayment plan, especially curated for salaried borrowers in India, to help eliminate ₹10 lakh debt efficiently.

Break Down Your ₹10 Lakh EMI-Based Debt

Understanding the composition of your ₹10 lakh debt is the first and most important step. Different loans carry different interest rates and repayment conditions.

Typical EMI-Based Debt Structure:

| Loan Type | Amount | Interest Rate (avg) | Monthly EMI (5 years) |

| Personal Loan | ₹6,00,000 | 11% – 15% | ₹13,000 – ₹14,300 |

| Consumer Durable Loan | ₹2,00,000 | 16% – 18% | ₹4,500 – ₹5,000 |

| BNPL / Short-Term Loan | ₹2,00,000 | 18% – 24% | ₹5,000 – ₹6,200 |

Total EMI outgo can be ₹22,000 to ₹26,000/month across 3–4 lenders—making it difficult to manage both finances and timelines.

Step 1: List All Your Active Loans with EMI Details

Start by creating a basic loan tracker with:

- Loan provider name

- Remaining balance

- Interest rate

- EMI amount

- End date of repayment

This will give you visibility on which loans need immediate attention.

RupeeQ Tip:

Use RupeeQ’s free credit score tool to pull up your complete loan summary linked to your PAN. It helps detect even inactive or low-balance loans you may have missed.

Step 2: Choose the Right Repayment Strategy

There are two tried-and-tested methods to attack multiple EMI-based debts:

1. Avalanche Method (Interest Priority):

Start by paying extra on the loan with the highest interest rate while maintaining minimum payments on the others.

2. Snowball Method (Balance Priority):

Clear the loan with the smallest outstanding amount first to reduce the number of EMIs and build momentum.

Which should you use?

- Choose Avalanche if saving on interest is your main goal.

- Choose Snowball if you want psychological wins early on.

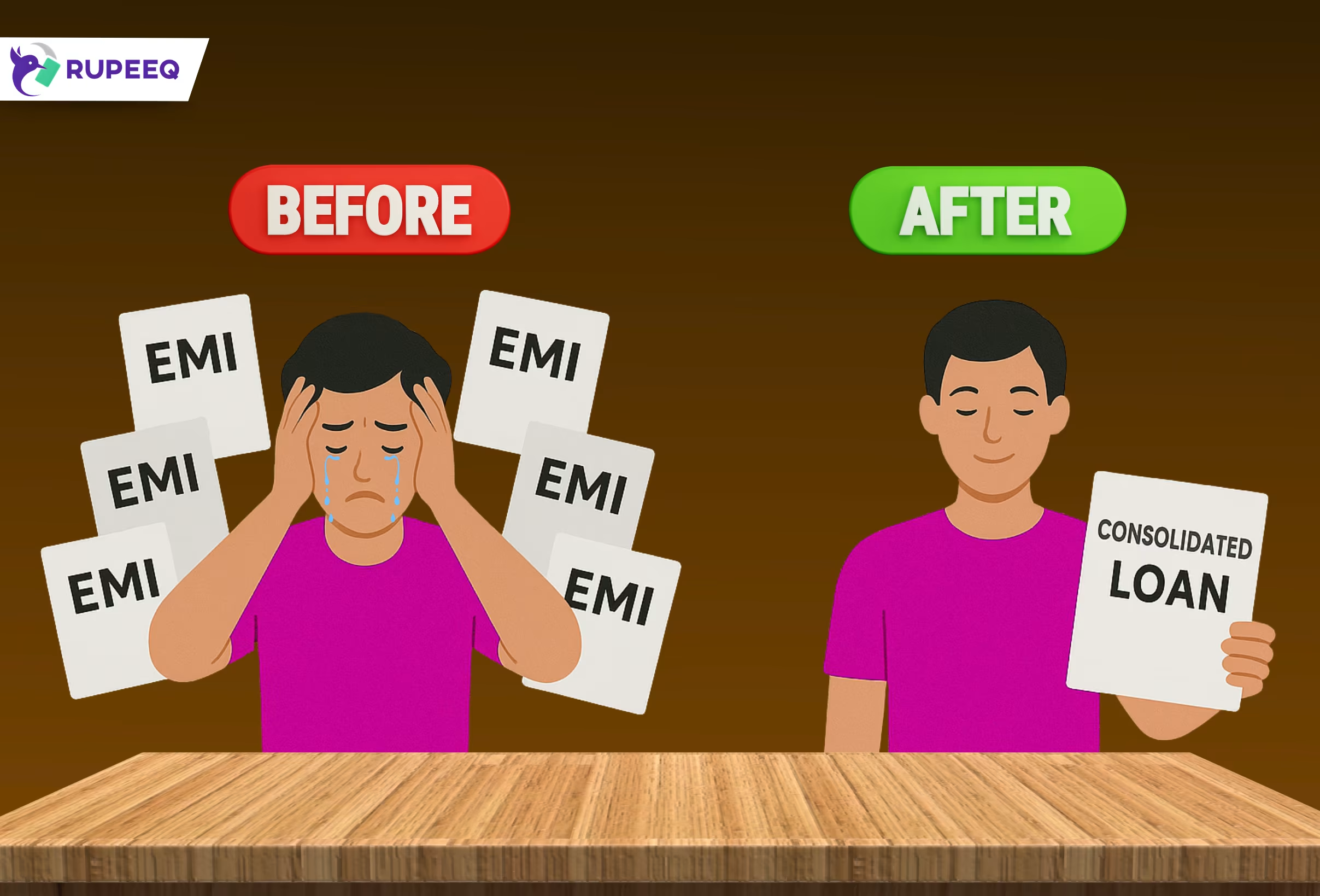

Step 3: Consolidate All Loans into One EMI

If you’re juggling multiple EMIs, debt consolidation can simplify your life. This means taking a single personal loan (up to ₹10L) at a lower interest rate to close all other active loans.

Benefits of Loan Consolidation:

- One fixed EMI per month

- Better rate than BNPL or consumer loans

- More predictable repayment tenure

| Before Consolidation | After Consolidation |

| 3–4 different EMIs | 1 consolidated EMI |

| Multiple due dates | Single due date |

| 16–24% blended interest rate | 11% – 14% interest possible |

| ₹25,000 EMI outgo (approx) | ₹20,000–₹22,000 EMI (approx) |

RupeeQ Tip:

Check eligible offers on RupeeQ before applying. You might get consolidation offers based on your credit score and salary, with minimal documentation.

Step 4: Rework Your Monthly Budget

If your EMI burden is too high, reallocate your spending. Identify areas where you can save:

- Weekend outings

- OTT subscriptions

- EMI-based electronics

- Lifestyle expenses

Use this margin to increase your monthly payment or build a prepayment fund.

Step 5: Use Extra Income Wisely

Every additional ₹5,000–₹10,000 earned per month can help close your debt much faster. Try these:

- Weekend freelance gigs

- Part-time tutoring

- Asset rental (bike, storage, etc.)

- Cashback and bonus redirection

Instead of spending bonuses, use them for lump-sum prepayments to reduce interest costs and loan tenure.

Step 6: Automate EMI Payments

Missing even one EMI could result in penalties and lower credit scores. Avoid that risk by:

- Setting auto-debit mandates via net banking

- Using UPI standing instructions

- Maintaining sufficient balance by 3rd or 4th of every month

RupeeQ Tip:

Check your credit report monthly to ensure EMIs are being reported correctly by all lenders.

Step 7: Consider Prepayment Every 6 Months

Many personal loans allow free prepayment after 12 months. Use this to your advantage.

Sample Scenario:

If your consolidated EMI is ₹22,000 for 5 years, but you prepay ₹1 lakh at the end of year 1, your tenure may reduce by 8–10 months and total interest saved could be ₹20,000–₹30,000.

Ask your lender if partial or full prepayment is allowed without charges.

Step 8: Monitor Your Progress

Track your progress every month:

- Outstanding balance

- Prepayment targets met

- Credit score improvement

- EMI-to-income ratio

This keeps you motivated and accountable.

Sample Timeline to Clear ₹10 Lakh Debt

| Scenario | Monthly EMI | Extra Monthly Payment | Time to Clear |

| Normal Repayment (5 years) | ₹22,000 | ₹0 | 60 months |

| With ₹5K Extra/Month | ₹22,000 | ₹5,000 | 43–45 months |

| With Annual ₹1L Prepayment | ₹22,000 | Bonus used yearly | 38–40 months |

Final Thoughts

Clearing a ₹10 lakh debt might seem challenging, but with planning and consolidation, it’s completely possible. Instead of dealing with multiple EMIs, one consolidated loan with a longer tenure and lower interest rate can bring relief—and discipline.

Stick to your plan, avoid new loans, and automate everything you can. You’ll be debt-free sooner than you think.