Handling multiple loan repayments can be challenging, especially if you have personal loans, home loans, car loans, credit card dues, and other debts to manage simultaneously. Missed EMIs or late payments can lead to penalty charges, higher interest costs, and a negative impact on your credit score.

Effectively managing multiple loan repayments requires strategic planning, financial discipline, and the right repayment approach to avoid financial stress. This blog provides practical strategies to manage multiple loan EMIs effectively, ensuring smooth repayment without affecting your financial stability.

Prioritize Your Loans Based on Interest Rates

When repaying multiple loans, it’s essential to prioritize them based on interest rates.

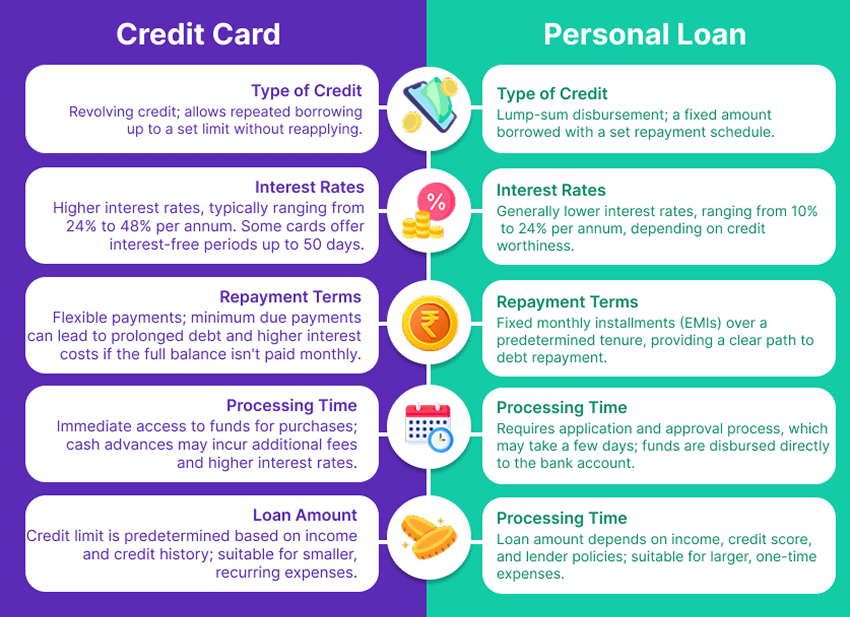

High-Interest vs. Low-Interest Loans

- High-interest loans (credit cards, personal loans) should be cleared first to reduce financial burden.

- Low-interest loans (home loans, education loans) can be managed over time since they have longer tenures and tax benefits.

Which Loan Should You Pay Off First?

- Credit Card Debt: The highest priority due to interest rates of 24-48% per annum.

- Personal Loan: Should be cleared next, especially if the interest rate is above 14%.

- Home Loan: Can be repaid over the tenure as it comes with tax benefits and lower interest rates (7-10%).

RupeeQ Tip – Use the Debt Avalanche Method—start repaying loans with the highest interest rate first, while making minimum payments on others. This reduces the overall cost of debt.

Consolidate Loans to Reduce EMI Burden

If handling multiple EMIs is overwhelming, consider loan consolidation to simplify repayments and reduce interest costs.

What is Loan Consolidation?

It involves combining multiple high-interest loans into a single loan with a lower interest rate, reducing the number of EMIs and overall financial strain.

How to Consolidate Your Loans?

- Personal Loan Balance Transfer: Shift your existing personal loan to another lender at a lower interest rate.

- Debt Consolidation Loan: Take a new loan to clear multiple debts, replacing them with a single EMI.

- Loan Against Property: If you own property, leverage it for a low-interest secured loan to consolidate debts.

When Should You Consider Loan Consolidation?

- When you have multiple high-interest loans (personal loans, credit cards, payday loans).

- If your EMIs exceed 40% of your income, making repayment difficult.

- If your credit score allows you to qualify for a lower-interest loan.

Automate Your Loan Repayments

Missing EMI payments can lead to late fees, penalty charges, and credit score damage. Setting up automatic payments ensures that EMIs are paid on time.

How to Automate Your EMI Payments?

- Use Auto-Debit Facility: Enable standing instructions with your bank for EMI deductions.

- Set Up Payment Reminders: Use financial apps to track due dates and ensure timely payments.

- Use NACH Mandate: Authorize your lender to debit EMIs directly from your account.

Create a Loan Repayment Budget

A well-planned loan repayment budget helps ensure that you can manage multiple EMIs without financial stress.

Steps to Create a Loan Budget:

- List All Loans & EMIs: Note down the loan type, EMI amount, due date, and remaining tenure.

- Track Income & Expenses: Ensure EMIs do not exceed 40-50% of your monthly income.

- Reduce Unnecessary Expenses: Cut discretionary spending to allocate more funds for loan repayments.

- Build an Emergency Fund: Keep at least 3-6 months of EMIs saved to cover unexpected situations.

RupeeQ Tip – If your EMI burden is too high, consider prepaying high-interest loans in small amounts to reduce outstanding debt faster.

Use the Debt Snowball or Avalanche Method

Different repayment strategies can help you clear multiple loans systematically.

Debt Snowball Method

- Pay off the smallest instant personal loan first, then move to the next.

- Provides quick wins and motivates faster repayment.

Debt Avalanche Method

- Pay off the loan with the highest interest rate first.

- Helps reduce overall interest costs faster.

Which Method is Best?

- Use Snowball if you need motivation to stay committed to loan repayments.

- Use Avalanche if you want to save the most money on interest over time.

Consider Prepayment or Foreclosure to Reduce Debt Faster

If you have surplus income, consider prepaying or foreclosing your loans to reduce your total debt.

Benefits of Prepayment:

- Reduces total interest outgo.

- Lowers EMI burden for future months.

- Helps close high-cost loans earlier.

Things to Check Before Prepayment:

- Some lenders charge prepayment penalties (1-3%).

- Prepayment is more beneficial for high-interest loans.

- Always check if your savings from prepayment outweigh the penalty.

RupeeQ Tip – If you have a home loan or personal loan, check the prepayment terms to see if paying off early can save you money.

Improve Your Credit Score for Better Loan Terms

A high credit score (750+) helps you qualify for lower interest rates, better repayment terms, and refinancing options.

How to Improve Your Credit Score?

- Pay EMIs on time without delays.

- Keep your credit utilization below 30%.

- Avoid multiple loan applications in a short period.

- Check your credit report for errors and correct any discrepancies.

RupeeQ Tip – Use RupeeQ ACE to check your credit score for free and get tips on improving your financial profile.

Avoid Taking New Loans Until Existing Debts Are Cleared

While managing multiple EMIs, avoid taking additional loans unless absolutely necessary.

Why Should You Avoid New Loans?

- Increases debt burden, making repayments harder.

- Leads to a higher debt-to-income ratio (DTI), affecting future loan eligibility.

- Too many loans can lower your credit score.

Final Thoughts: Manage Your Loan Repayments Smartly

Handling multiple loan repayments requires a disciplined approach, careful budgeting, and strategic repayment planning. By prioritizing loans, consolidating debts, and using automated payments, you can reduce financial stress and improve repayment efficiency.

Key Takeaways:

- Prioritize high-interest loans first to minimize interest costs.

- Consolidate debts into one lower-interest loan if possible.

- Automate EMI payments to avoid late fees and credit score damage.

- Create a loan repayment budget to track and manage all dues effectively.

- Use the Debt Avalanche or Snowball Method based on your repayment goals.

- Improve your credit score to get better loan refinancing options.

- Avoid new loans until existing debts are under control.

If you’re struggling with multiple loan repayments, compare refinancing and balance transfer options on RupeeQ today to reduce your financial burden.