Debt consolidation is often marketed as a smart solution for managing multiple loans. But is it really the right move for you? The answer depends on your financial situation, the types of loans you carry, and your goals. In this blog, we’ll help you understand when debt consolidation makes sense, what benefits it offers, and when you should reconsider. By the end, you’ll have clarity on whether consolidating your debt is a good idea for your unique circumstances.

What is Debt Consolidation?

Debt consolidation means combining multiple existing loans into a single loan—usually a personal loan—so that you repay just one EMI instead of many. This new loan covers your total outstanding debt and is repaid over a new tenure at a potentially better interest rate.

For example, if you’re currently paying three separate EMIs for three different loans, a consolidation loan can merge them into one EMI—simplifying your monthly obligations.

When is Debt Consolidation a Good Idea?

Debt consolidation can be very effective in certain financial scenarios. If any of the following applies to you, it might be a wise decision.

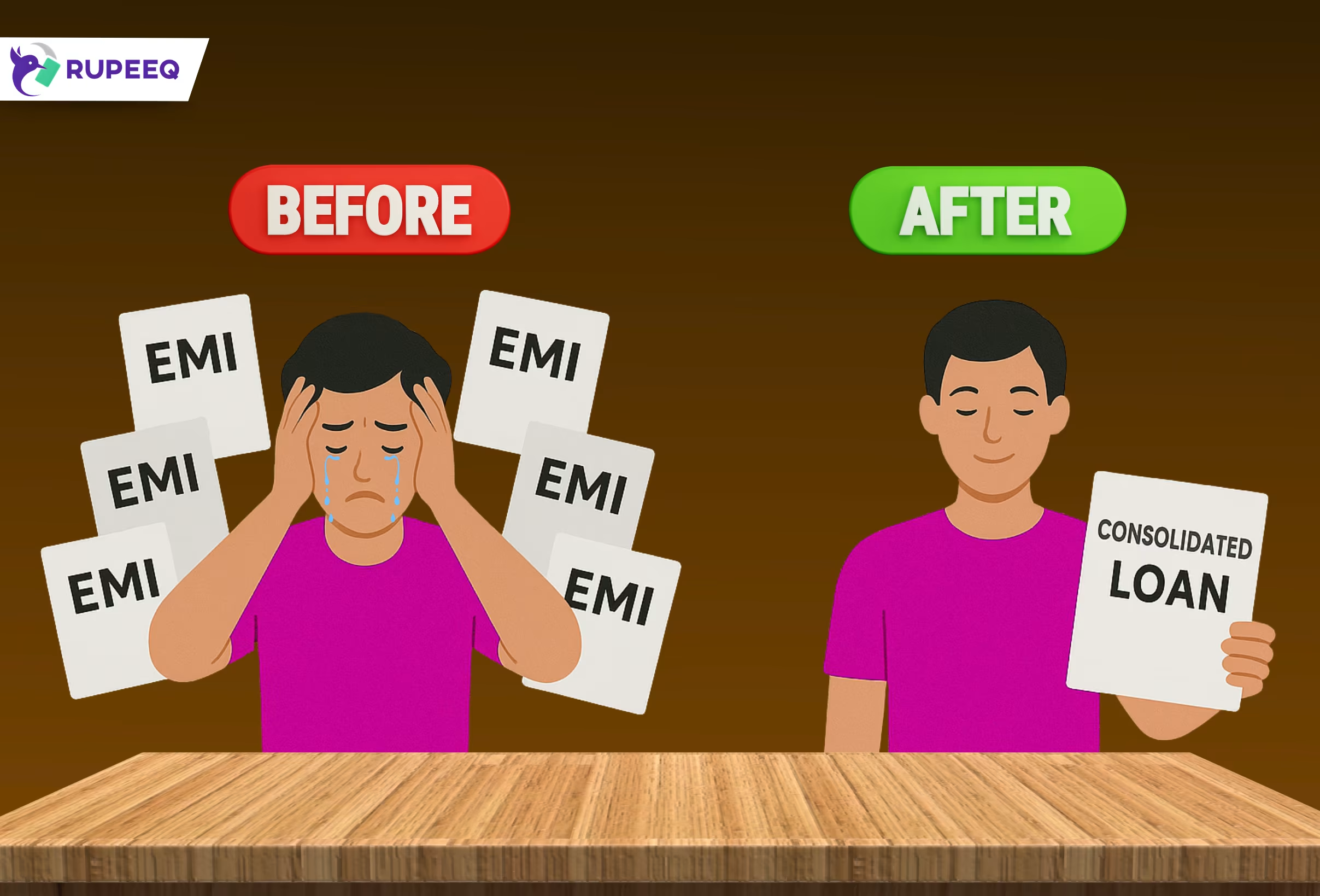

1. You’re Struggling to Manage Multiple EMIs

If your monthly calendar is filled with different EMI dates and amounts, it increases the risk of missing payments. This not only attracts penalties but also hurts your credit score.

Why consolidation helps:

You pay one fixed EMI, on one fixed date, to one lender. This simplifies financial planning and reduces stress.

2. You’re Paying High Interest on Existing Loans

Sometimes borrowers end up with high-interest loans due to poor credit history or urgent needs. Over time, these loans eat into your income and savings.

Why consolidation helps:

You may qualify for a personal loan at a lower interest rate, especially if your credit score has improved. Replacing costlier loans can reduce your total interest outgo.

RupeeQ Tip: Check multiple pre-approved consolidation loan offers on RupeeQ to get the best available rate for your profile.

3. You Want to Improve Your Cash Flow

If a large chunk of your salary goes into loan repayments, it leaves little room for savings or emergencies. This can push you into further debt if unexpected expenses arise.

Why consolidation helps:

You can extend your loan tenure to lower your monthly EMI, easing your monthly cash flow. This gives you more breathing space in your budget.

4. You’re Trying to Rebuild Your Credit Score

A poor credit score due to missed or delayed EMIs can make it harder to get fresh credit. Consolidation offers a second chance to rebuild your repayment history.

Why consolidation helps:

Managing a single loan is easier. Regular, on-time payments on the consolidated loan will gradually improve your credit score.

5. You Have an Unstable or Irregular Income

Freelancers, self-employed individuals, or those with seasonal income might find it hard to track and repay multiple loans.

Why consolidation helps:

One predictable EMI, rather than several, makes it easier to align repayments with cash inflow cycles.

When Debt Consolidation May Not Be a Good Idea

While consolidation has its benefits, it is not ideal in every case. Here are scenarios where you should avoid or delay debt consolidation.

1. You Have Only One or Two Loans

If your debt is already minimal and manageable, consolidation may be unnecessary. It might add processing fees or lead to a longer repayment cycle.

Better alternative:

Continue repaying your existing loans as scheduled. Focus on early closure rather than taking a new loan.

2. You’re Being Offered a Higher Interest Rate

If your credit score is poor, you may only qualify for a consolidation loan at a higher interest rate than your current loans.

Why it’s risky:

You may reduce your EMI slightly by extending tenure, but end up paying much more in interest over time.

3. You Tend to Overspend After Loan Closure

Some people see consolidation as a reset and fall into the trap of borrowing again soon after. This can result in a dangerous cycle of debt accumulation.

Important note:

Consolidation should come with a commitment to financial discipline. If you continue to spend recklessly, your debt will only grow.

4. You’re Near the End of Your Loan Tenure

If you have just a few EMIs left on your existing loans, consolidating them into a new long-term loan doesn’t make sense.

Why it’s a bad idea:

You’ll extend the repayment period unnecessarily and pay more in the long run.

Table: Pros and Cons of Debt Consolidation

| Pros | Cons |

| Simplifies monthly repayment | May involve processing fees |

| Can lower interest rates | May not be helpful for short-term debts |

| Improves credit score if managed well | Requires good credit to get best rates |

| Eases monthly cash flow | Can lead to overborrowing if not disciplined |

How to Decide If You Should Consolidate

Ask yourself the following questions before deciding:

- Do I have more than two active loans?

- Am I struggling to manage EMIs or missing payments?

- Is my credit score good enough for a low-rate loan?

- Do I plan to avoid taking new debt after consolidation?

- Am I clear on the total cost of the new loan?

If the answers are mostly “Yes,” then consolidating your debt is likely a good idea.

How RupeeQ Helps You Consolidate Smartly

RupeeQ is designed to make the debt consolidation process simpler, faster, and smarter. Here’s how:

- Free credit score check to know your eligibility

- Multiple lender offers in one place

- Personalized loan options based on your profile

- EMI calculator to compare tenure and repayment plans

- Digital application and paperless process

RupeeQ Tip: Before you apply, run a quick debt consolidation analysis on RupeeQ to see your best-fit offers and potential savings.

Final Thoughts

So, is it a good idea to consolidate your debt? Yes—if done at the right time, with the right loan, and for the right reasons. It can simplify your life, lower your stress, and even improve your creditworthiness. But it’s not a shortcut to avoid debt—it’s a tool to manage it better.

Approach consolidation as a financial reset, not a license to borrow more. Combine it with discipline, budgeting, and responsible repayment to get the most out of it.

Want to simplify your EMIs?

Visit RupeeQ.com to check your credit score, view customized loan consolidation options, and start your journey to a debt-free future—all in one place.