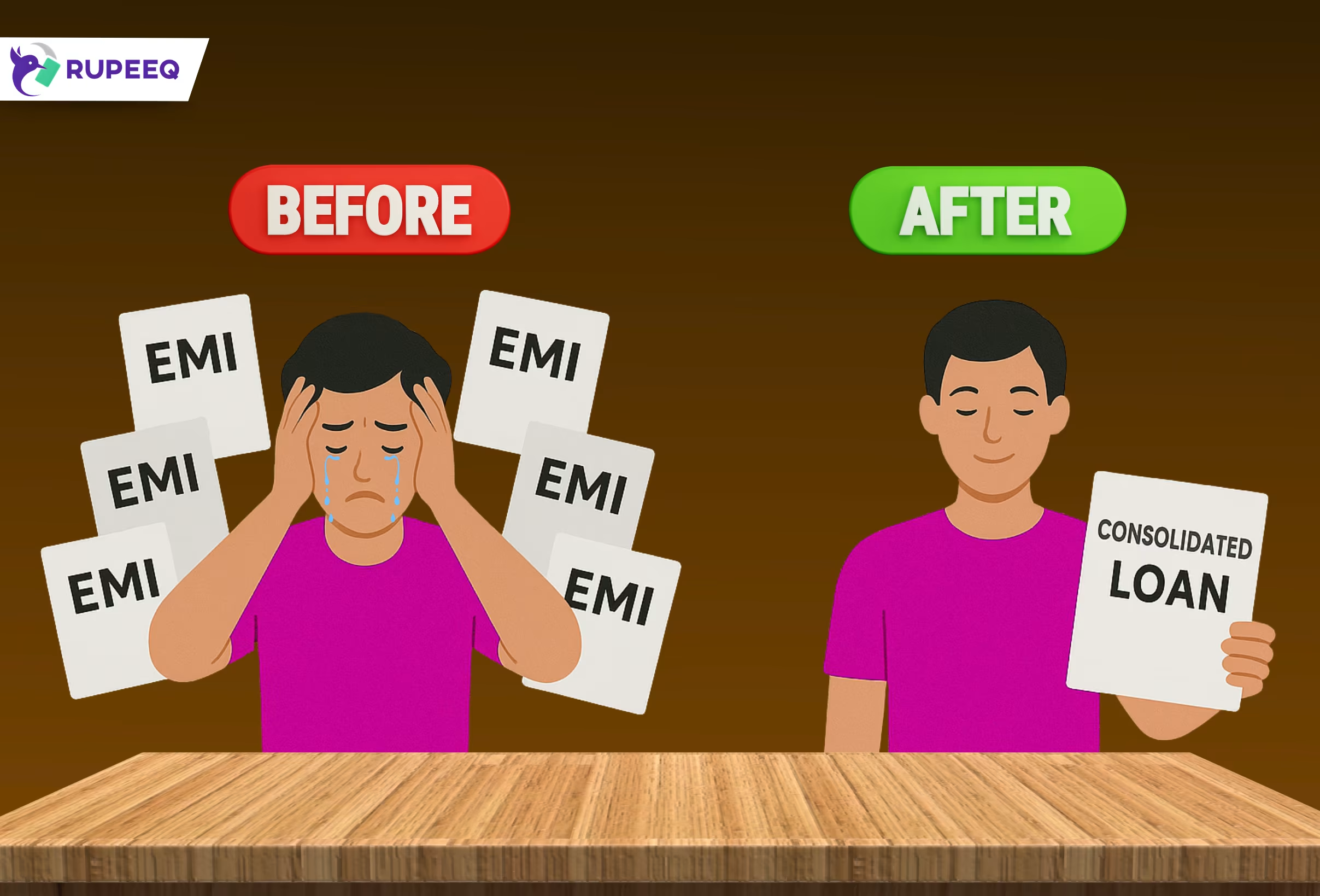

Debt consolidation can be a smart financial decision if you are struggling with multiple loan EMIs. It allows you to merge several outstanding loans into one and repay through a single EMI every month. However, the benefits of debt consolidation can be lost if you commit certain avoidable mistakes. In this blog, we’ll walk you through the most common mistakes people make while applying for a debt consolidation loan—and how you can avoid them to ensure a stress-free borrowing experience.

1. Failing to Review All Existing Loans Before Consolidation

One of the first and most common mistakes borrowers make is not having a complete understanding of their current loan liabilities. Before applying for debt consolidation loan, it’s important to review all your active loans.

You must note:

- The outstanding principal for each loan

- Interest rates charged

- Tenure and remaining EMIs

- Any foreclosure or prepayment charges

Without this basic groundwork, you may end up taking a consolidation loan of the wrong amount or unnecessarily clubbing loans that were already manageable.

2. Consolidating Loans With Low Interest or Short Tenure

Debt consolidation is most effective when used to replace high-interest or difficult-to-manage loans. However, some borrowers make the mistake of including low-interest loans or those with just a few EMIs left.

This can result in:

- Increased repayment timeline

- Higher overall interest payout

- Less financial benefit from consolidation

Be selective about which loans to include in the consolidation. Avoid extending debt unnecessarily. RupeeQ Tip: Use the RupeeQ ACE to identify which of your loans actually need consolidation and which can be paid off separately.

3. Ignoring the Total Cost of a Debt Consolidation Loan

Many borrowers focus only on the new EMI amount, assuming that a lower EMI is always better. But this is not always true.

You must consider:

- Processing fees

- Foreclosure charges on old loans

- Interest rate of the new loan

- New loan tenure and total interest payable

A longer loan term with a lower EMI may increase your total repayment amount significantly.

4. Not Comparing Consolidation Loan Offers from Multiple Lenders

Each lender offers different interest rates, processing fees, and repayment options. Choosing the first available loan without comparison can lead to missed opportunities.

To get the best deal, compare:

- Interest rates

- Tenure flexibility

- Prepayment and foreclosure rules

- Disbursal speed and documentation requirements

RupeeQ Tip: RupeeQ lets you view and compare multiple debt consolidation loan offers from top lenders in one place—without affecting your credit score.

5. Applying Without Checking Your Credit Score First

Your credit score is a critical factor in loan approval, interest rates, and the amount you can borrow. Applying without knowing your score is a risky move that may lead to loan rejection or high interest charges.

Ideally, check your score in advance and take steps to improve it if it’s below 700.

RupeeQ Tip: You can check your credit score for free on RupeeQ and get suggestions to improve it before you apply.

6. Borrowing More Than You Actually Need

Another mistake is applying for a loan amount that is higher than required. Many borrowers think it’s better to have extra funds for other expenses, but this can lead to a higher EMI burden and longer debt cycle.

Only borrow enough to pay off your existing loans. Avoid taking on new debt unless absolutely necessary.

7. Choosing the Longest Tenure for Lower EMI

It’s tempting to choose the longest tenure to reduce your EMI. While this may help in the short term, it increases the total interest you pay over the life of the loan.

Instead, try to strike a balance between EMI affordability and tenure length. Use an EMI calculator to simulate different scenarios.

8. Overlooking the Terms and Conditions of the Loan

Some borrowers do not read the fine print and end up facing hidden charges, strict prepayment rules, or penalties.

Always check:

- Processing and documentation fees

- Foreclosure or part-payment rules

- Penalty for delayed EMI

- Lock-in periods

Understanding the terms helps you avoid surprises and manage the loan better.

9. Submitting Multiple Loan Applications at the Same Time

Applying to several lenders at once may seem like a good idea to increase your chances, but it can hurt your credit score. Each application triggers a hard enquiry, which reduces your score and makes you appear credit-hungry.

Instead of applying individually, use a loan marketplace.

10. Providing Incomplete or Incorrect Documentation

Loan delays or rejections are often caused by errors in documentation. Wrong information, outdated financial records, or mismatched identity documents can delay the process or even lead to rejections.

Before you apply, make sure:

- All KYC documents are up to date

- Income proofs (salary slips or ITRs) are recent

- Bank statements are clear and complete

Accurate documentation ensures smooth loan processing.

11. Not Having a Post-Consolidation Repayment Plan

Taking the loan is only part of the process. Without a solid repayment plan, you may default again and hurt your credit score further.

After consolidation:

- Adjust your monthly budget to accommodate the new EMI

- Set up auto-debit from your account

- Track payments and avoid new loan applications until this one is closed

Summary Table: Mistakes to Avoid During Debt Consolidation Loan Application

| Mistake | Why It’s a Problem |

| Not reviewing current loans | May borrow wrong amount or include unnecessary loans |

| Consolidating low-interest loans | Increases cost without benefit |

| Ignoring total cost | Higher interest burden over time |

| Not comparing lenders | Missed opportunity for better rates |

| Skipping credit check | Risk of rejection or high rates |

| Over-borrowing | Increases debt unnecessarily |

| Choosing long tenure blindly | More interest paid overall |

| Not reading fine print | Hidden charges or inflexible terms |

| Applying to multiple lenders | Damages credit score |

| Incomplete documentation | Causes delays or rejection |

| No repayment plan | Increases risk of default again |

Steer Clear of These Mistakes for Best Debt Consolidation

A debt consolidation loan can be a smart financial move—only if approached with planning and caution. Avoiding the mistakes listed above will help you make the most of the opportunity to simplify your loan repayment, reduce financial stress, and rebuild your credit profile.

If you’re considering loan consolidation, RupeeQ offers a seamless digital platform to check your credit score, explore pre-approved offers, and apply for the best-fit loan—all in one place.

Visit RupeeQ.com today and take the first step toward simplifying your debt with confidence.