Your CRIF credit report is one of the most important documents lenders use to evaluate your creditworthiness. But like any data-driven system, errors can occur—whether it’s a loan marked as active even after closure, a wrong EMI status, or an account you don’t recognize.

These errors can lower your credit score and hurt your chances of getting a loan or credit card on favorable terms. The good news is, you have the right to dispute and correct any errors in your CRIF credit report.

In this blog, we’ll walk you through the exact steps to dispute errors in your CRIF report, how long it takes, and how RupeeQ can simplify the process for you.

Why Disputing Errors Is Important

Even a single wrong entry in your CRIF report can lead to:

- Lower credit score

- Loan rejections or delays

- Higher interest rates

- Reduced credit limit approvals

- Negative impact on financial reputation

RupeeQ Tip: Check your CRIF credit report every 3–6 months using RupeeQ ACE. It’s free and gives you insights into what’s helping or hurting your score.

Common Errors Found in CRIF Credit Reports

Before we look at the steps, here are common mistakes you should look for:

- Incorrect personal details (name, PAN, date of birth, contact information)

- Loan or credit card marked as active even after full repayment

- Wrong repayment history (EMI marked late despite timely payment)

- Duplicate accounts listed for the same loan

- Accounts you never opened (possible fraud or identity theft)

- Incorrect Days Past Due (DPD) entries

- Wrong account status (settled vs. closed)

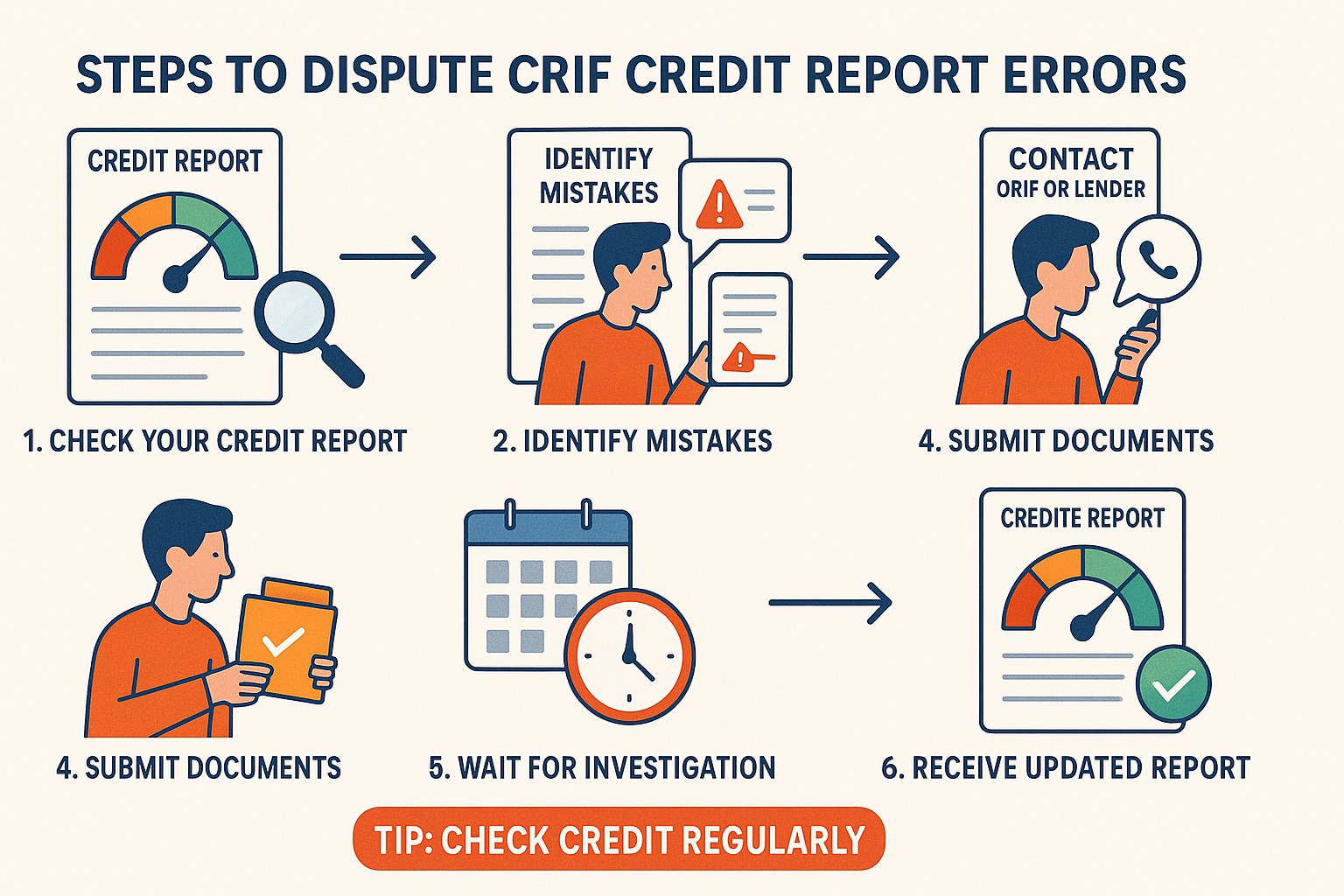

Steps to Dispute Errors in Your CRIF Credit Report

You can raise a dispute through RupeeQ or directly with CRIF High Mark.

Step 1: Review Your CRIF Report Carefully

- Check your report section by section:

- Personal Information – Ensure all details match your official records

- Account Information – Verify account type, status, and balances

- Repayment History (DPD) – Confirm “000” entries for timely payments

- Enquiries – Ensure all enquiries were initiated by you

- Highlight any discrepancies you notice.

Step 2: Gather Supporting Documents

You’ll need to provide proof for your dispute. Examples include:

- Loan closure letter or NOC (No Objection Certificate)

- Payment receipts or bank statements

- Correct PAN card or ID proof (for personal detail errors)

Step 3: Raise a Dispute

Option A: Through RupeeQ

If you’ve accessed your report through RupeeQ:

- Log in to RupeeQ.com

- Go to My Report

- Click Raise a Query

- Select the report and specific account or field to correct

- Upload relevant documents

- Submit the request

Option B: Directly with CRIF High Mark

- Visit www.crifhighmark.com

- Click on My Report

- Select Raise a Query

- Choose the incorrect account or information

- Upload supporting documents

- Submit the dispute form

Step 4: Track Your Dispute

- You will receive a ticket number by email (keep it for reference).

- Use this to track the status of your dispute on the RupeeQ dashboard or CRIF website.

Step 5: Resolution Timeline

- CRIF will investigate with the concerned lender.

- They must provide a resolution within 30 calendar days.

- If the dispute is valid, your credit report will be updated in the next reporting cycle.

RupeeQ Tip: Check your report again 30–45 days after resolution to confirm the correction has been applied.

What to Do If the Dispute Isn’t Resolved

If you don’t receive a satisfactory resolution:

- Contact the lender directly to update their records with CRIF.

- Raise the issue with CRIF’s Grievance Redressal Officer (details on CRIF website).

- Escalate to RBI’s Ombudsman if neither resolves the matter.

Quick Summary: Dispute Process at a Glance

| Step | Action |

| Review report | Identify errors in each section |

| Gather proof | NOC, receipts, ID documents |

| Raise dispute | Via RupeeQ or CRIF website |

| Receive ticket number | For tracking resolution |

| Resolution | Within 30 days |

| Verify update | Recheck your report after 30–45 days |

Final Thoughts

Errors in your CRIF credit report aren’t just inconvenient—they can cost you financially. Fortunately, the dispute process is free, transparent, and time-bound.

With RupeeQ, you can:

- Check your CRIF credit score for free

- Review your credit report in detail

- Raise disputes in just a few clicks

- Track resolution progress without hassle

Taking a few minutes to dispute errors can improve your credit score, protect your creditworthiness, and make loan approvals easier.

FAQs

- Is there a fee to dispute CRIF report errors?

No. Disputing errors with CRIF or through RupeeQ is completely free. - How long does it take to correct an error?

Usually within 30 days, with changes reflected in the next monthly update. - Will my credit score improve after a dispute?

Yes, if the error was negatively affecting your score, it will improve once corrected. - Do I need to contact my lender separately?

CRIF will coordinate with your lender, but you can reach out directly if the dispute isn’t resolved. - Can I raise multiple disputes at once?

Yes, you can dispute all errors found in a single session.