Short Term Personal Loans (STPLs) are growing in popularity among salaried professionals, freelancers, and even small business owners. Designed for quick, small-ticket borrowing with tenures usually ranging from 3 to 12 months, these loans serve various needs—from emergency medical bills to managing sudden travel plans. However, several misconceptions still hold people back from making informed decisions.

In this blog, we’ll bust the top 5 myths about short term loans and help you separate fact from fiction.

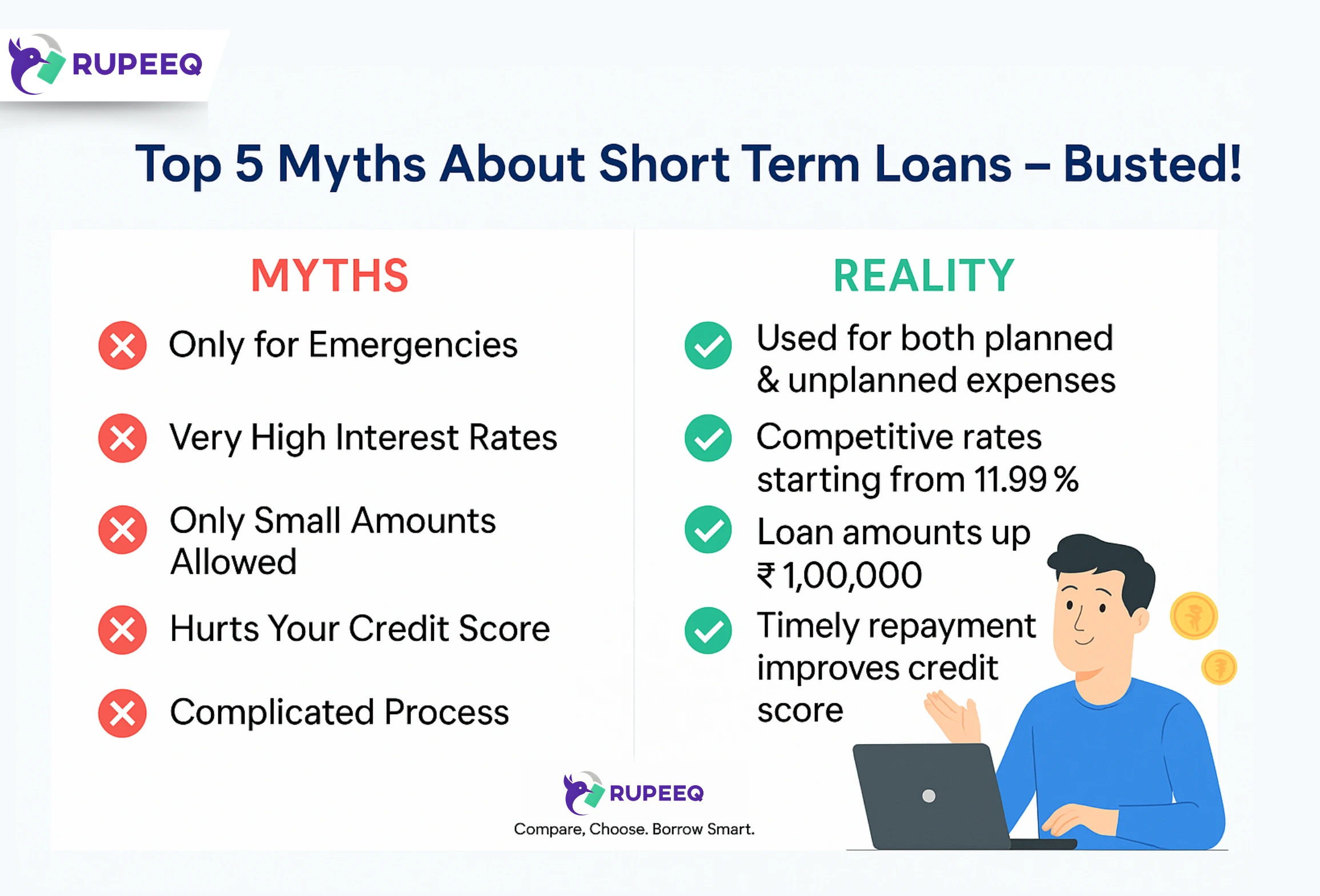

Myth 1: Short Term Loans Are Only for Emergencies

Many people think STPLs are meant only for dire medical needs or financial crises. While they are excellent for emergencies, that’s not their only use.

Reality:

STPLs are designed for planned as well as unplanned expenses—including vacations, gadget upgrades, course fees, festival spending, and more. Their flexibility and fast disbursal make them a handy financial tool even for proactive planning.

RupeeQ Tip:

Use short term loan comparison tool to find offers tailored to your specific need—whether it’s a vacation or wedding expense.

Myth 2: Short Term Loans Have Very High Interest Rates

There’s a common belief that since short term loans are unsecured, the interest rates are unreasonably high. This is only partially true.

Reality:

While some lenders may charge high rates, platforms like RupeeQ offer short term loans starting from 11.99% p.a. based on your credit profile. If you have a good repayment history, you can easily qualify for competitive rates.

| Credit Score Range | Approx. Interest Rate Range |

| 750+ | 11.99% – 16% p.a. |

| 700–749 | 14% – 20% p.a. |

| 650–699 | 18% – 24% p.a. |

RupeeQ Tip:

Check credit score for free before applying. You’ll see personalized offers that suit your credit profile.

Myth 3: You Can Only Borrow a Small Amount

Some borrowers assume that short term loans are limited to ₹10,000–₹25,000, making them unfit for mid-size expenses.

Reality:

Short term personal loans on RupeeQ can go up to ₹1 lakh, depending on your income and creditworthiness. Many lenders offer flexible ticket sizes—from ₹5,000 to ₹1,00,000—making them useful for both minor and moderate expenses.

Use Cases for Different Loan Sizes:

| Purpose | Loan Amount |

| Doctor visit | ₹10,000 |

| Appliance purchase | ₹25,000 |

| School admission fee | ₹40,000 |

| Wedding expenses | ₹75,000 |

| Travel & stay | ₹1,00,000 |

Myth 4: STPLs Harm Your Credit Score

A lot of people avoid taking short term loans because they believe it might negatively impact their credit score.

Reality:

A short term loan does not harm your credit score if you repay on time. In fact, timely repayment of even small-ticket loans adds to your positive credit history and improves your score over time. What causes damage is delayed payments or defaults.

RupeeQ Tip:

Opt for auto-debit repayment mode and choose a realistic EMI amount. Even repaying a ₹10,000 loan on time can build your credit profile.

Myth 5: It’s Complicated to Apply for a Short Term Loan Online

Some borrowers still believe they need to visit banks, fill long forms, and provide multiple documents to get any loan, even a small one.

Reality:

Applying for an STPL via platforms like RupeeQ is 100% online, paperless, and can be completed in minutes. All you need is your PAN, Aadhaar, bank statement, and salary proof. Approval and disbursal often happen within 24–48 hours.

How It Works:

- Visit RupeeQ’s STPL page

- Enter basic details and check loan eligibility

- Compare offers from 15+ lenders

- Upload KYC and income documents

- Get loan approved and disbursed

Final Thoughts

Short Term Personal Loans are not what they used to be a decade ago. With fintech platforms like RupeeQ making borrowing easy, fast, and personalized, it’s time to unlearn these outdated myths. Whether you need money for a medical need or a mid-year vacation, STPLs can be the smart, structured, and secure solution you’ve been looking for.

Use short term loans smartly and sparingly. Don’t borrow more than you need, and always plan your repayments in advance to avoid debt traps.