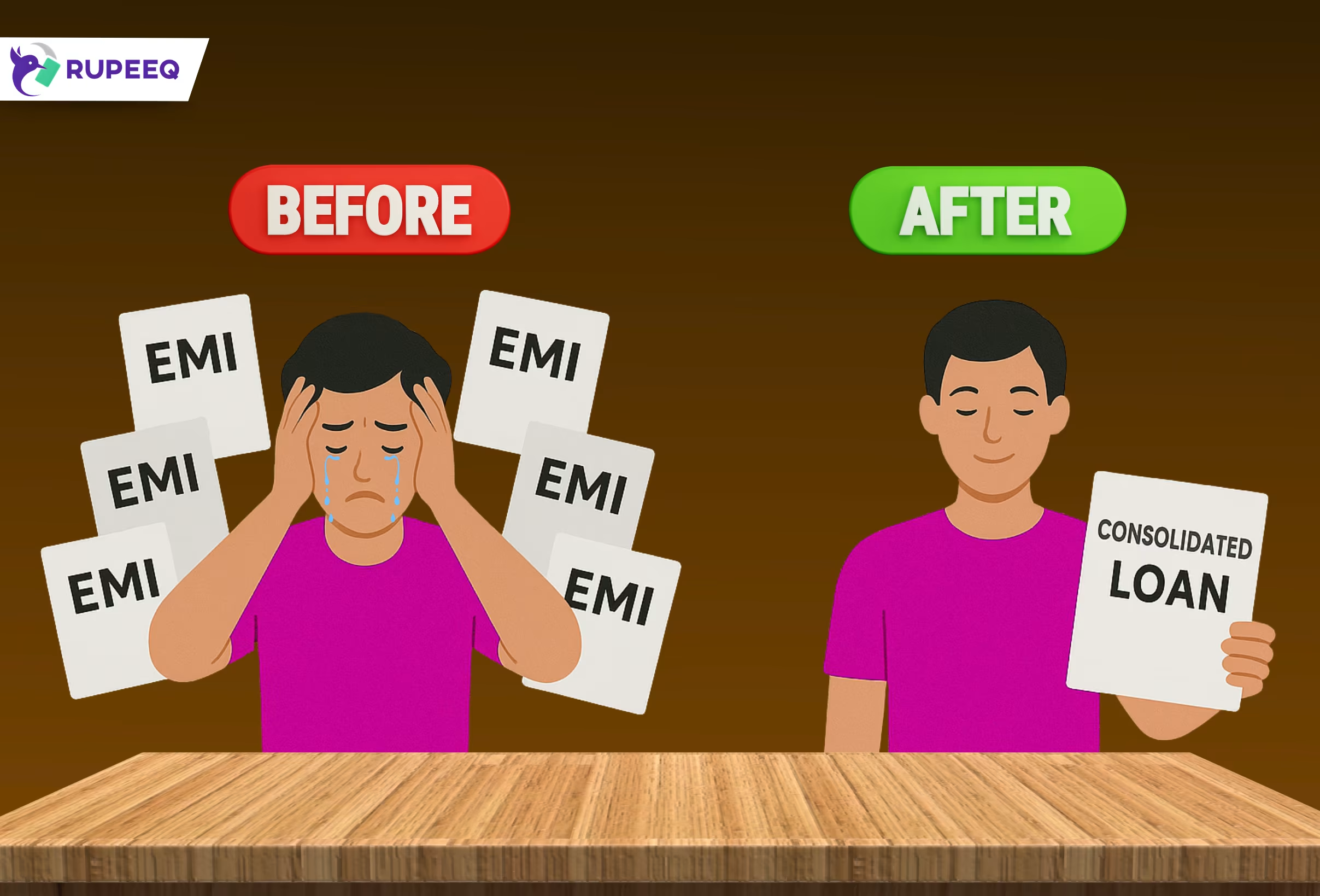

Debt consolidation is a powerful financial strategy that helps you manage multiple loans by combining them into a single repayment plan. But like any financial decision, it requires careful planning and understanding. One way to evaluate whether debt consolidation is right for you, or whether you’ll be eligible for it, is through the 4 C’s framework: Credit, Capacity, Collateral, and Character. These four elements help lenders assess your creditworthiness and help you determine your readiness to apply.

In this blog, we’ll break down each of the 4 C’s and explain how they affect your debt consolidation journey.

Understanding the 4 C’s of Debt Consolidation

Before a lender approves your debt consolidation loan, they evaluate your profile on several parameters. These factors are commonly known in lending as the 4 C’s:

- Credit – Your credit score and history

- Capacity – Your income and repayment ability

- Collateral – Any asset offered as security

- Character – Your track record and intent to repay

Understanding how each of these works will help you improve your chances of loan approval and make smarter borrowing decisions.

1. Credit: The Foundation of Loan Approval

Credit refers to your credit score and your overall credit history. It’s the most important factor for unsecured debt consolidation loans, as it helps lenders gauge the level of risk in lending to you.

Why Credit Matters:

- A higher credit score (usually 700 and above) means better chances of loan approval.

- It also qualifies you for lower interest rates and better loan terms.

- Credit history reveals your past EMI behaviour, defaults, and loan closures.

How It Impacts Debt Consolidation:

If your credit score is high, you are likely to get a personal loan at a competitive interest rate to consolidate your debts. However, if your score is low (below 650), you might either be rejected or offered a loan at a very high interest rate, which defeats the purpose of consolidation.

RupeeQ Tip: Always check your credit score before applying. Use Free Credit Score Check to see where you stand and improve your score if needed.

2. Capacity: Your Ability to Repay the Loan

Capacity refers to your repayment ability—based on your monthly income, ongoing obligations, and financial stability. Lenders want to ensure that you can comfortably handle the EMI of the new consolidated loan.

How Lenders Evaluate Capacity:

- Income level (salary or business income)

- Monthly fixed obligations like EMIs and rent

- Debt-to-Income (DTI) ratio – Ideally below 40%

How It Impacts Debt Consolidation:

If your income is stable and your DTI ratio is healthy, lenders will be more confident in your repayment capacity. This improves your eligibility and strengthens your loan application.

Example:

If your monthly income is ₹50,000 and your existing EMIs total ₹25,000, your DTI is 50%—which is too high. But if you consolidate your loans and reduce the EMI to ₹15,000, your DTI improves to 30%, making your finances healthier.

RupeeQ Tip: Use personal loan EMI calculator to plan a tenure that keeps your EMI affordable and helps you maintain a good DTI ratio.

3. Collateral: Backing Your Loan with Security

Collateral is any asset you offer as security against the loan. While most debt consolidation loans are unsecured (especially personal loans), some borrowers may choose to pledge an asset like property, gold, or a fixed deposit to get better terms.

Why Collateral Can Be Helpful:

- Secured loans usually come with lower interest rates.

- You can borrow a higher loan amount against collateral.

- It helps people with poor credit scores qualify for consolidation.

How It Impacts Debt Consolidation:

If you own an asset that you can pledge, you may be eligible for a Loan Against Property (LAP) or a secured personal loan to consolidate your debts. However, this also increases the risk—if you default, the lender can seize the asset.

RupeeQ Tip: Choose a collateral-based loan only if you are confident about repayment. For most salaried users with good credit, an unsecured loan is faster and safer.

4. Character: Your Financial Behaviour and Intent

Character refers to your trustworthiness as a borrower. It may sound subjective, but lenders use data-driven insights to evaluate your intent and reliability.

Factors That Define Character:

- Past loan repayment history

- Number of loan applications in recent months

- Relationship with banks or NBFCs

- Stability of employment or business

- No history of willful default or fraudulent activity

How It Impacts Debt Consolidation:

Even with a decent credit score, lenders will review how you’ve handled loans in the past. Have you made timely payments? Have you closed loans responsibly? Have you bounced any cheques or delayed EMIs?

RupeeQ Tip: Avoid applying to multiple lenders at once. Instead, use RupeeQ to access multiple offers with one application and maintain a clean loan inquiry record.

Summary Table: The 4 C’s of Debt Consolidation

| C | Meaning | Why It Matters | Impact on Loan |

| Credit | Score & report | Shows creditworthiness | Affects approval and interest rate |

| Capacity | Income & EMI load | Shows repayment ability | Affects loan amount and tenure |

| Collateral | Asset offered | Lowers risk for lender | Improves eligibility and rate |

| Character | Past behaviour | Shows trustworthiness | Affects lender confidence |

How to Improve Your 4 C’s Before Applying

Here are a few simple steps you can take to strengthen your profile across all 4 areas:

- Credit: Pay EMIs on time, avoid maxing out credit cards, and check your score monthly.

- Capacity: Reduce non-essential expenses, avoid taking new loans, and maintain a good savings record.

- Collateral: Prepare valuation and legal documents if you’re pledging any asset.

- Character: Maintain financial discipline, limit loan applications, and don’t default—even if it’s a small amount.

RupeeQ Tip: Before applying, run a consolidation check on RupeeQ. It assesses your credit, capacity, and overall eligibility to match you with the right lenders.

Final Thoughts

The 4 C’s of debt consolidation—Credit, Capacity, Collateral, and Character—are not just lending jargon. They’re essential pillars that determine your success in securing a loan and managing your finances responsibly. Understanding how these factors work gives you the power to plan better, avoid rejections, and get the best possible deal when consolidating your debt.

Debt consolidation can simplify your life—but only when you’re financially prepared and well-informed.

Ready to Consolidate Your Loans?

Check your credit score, explore pre-approved offers, and compare debt consolidation options—only on RupeeQ.com. It’s 100% online, secure, and tailored to your credit profile.