Debt consolidation is often seen as a smart way to regain control over your finances when you’re dealing with multiple loan repayments. It not only helps simplify your debt but may also reduce your overall interest burden. But debt consolidation isn’t a one-size-fits-all solution. There are different ways to go about it, depending on your financial situation and the type of loans you’re carrying. In this blog, we’ll explain the three most common methods of debt consolidation, along with their pros, cons, and suitability for Indian borrowers.

Understanding Debt Consolidation: A Quick Overview

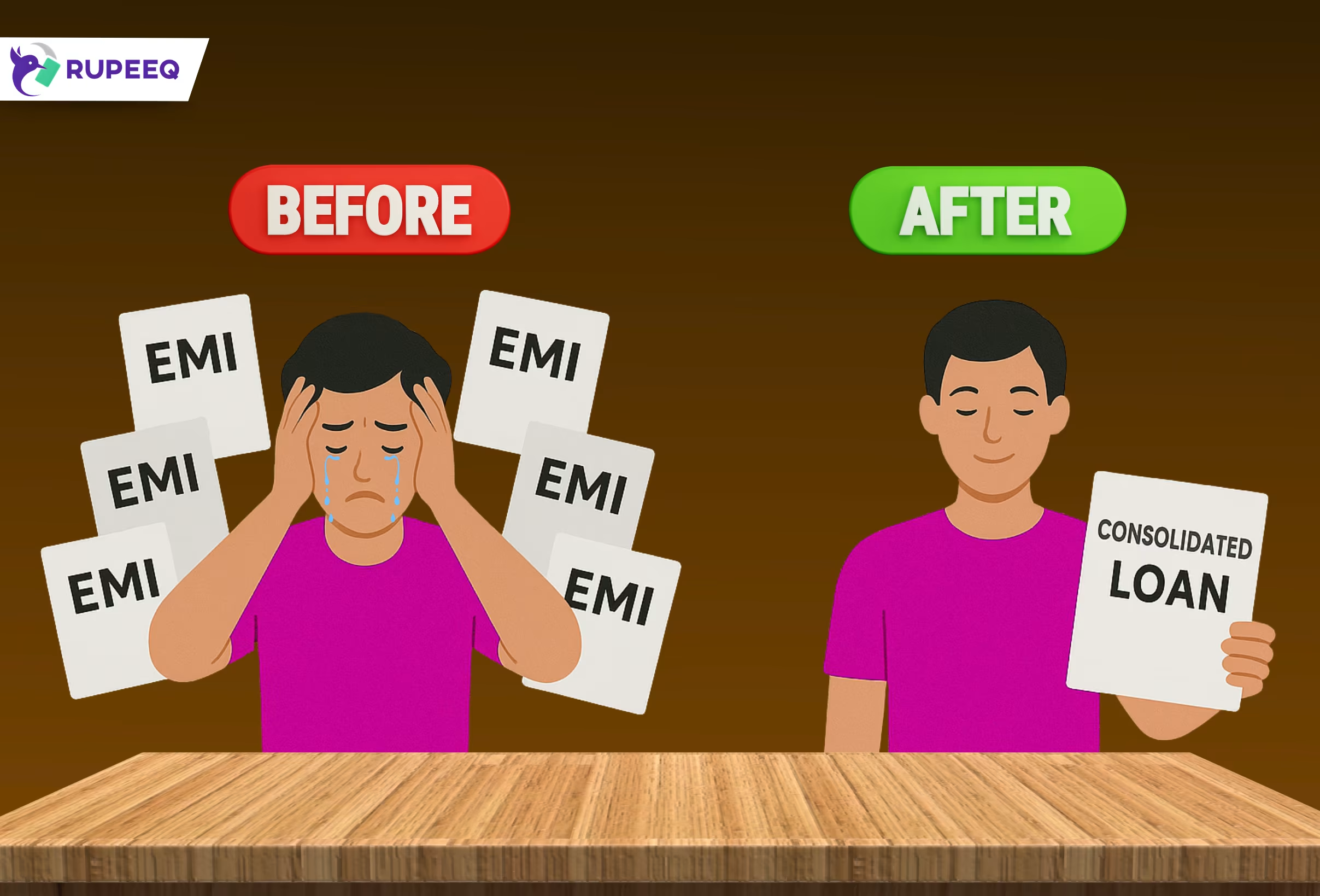

Debt consolidation refers to the process of combining multiple debts—such as personal loans, credit card dues, or short-term borrowings—into a single loan. The main goal is to make repayment easier by replacing multiple EMIs with just one.

There are three widely used methods of debt consolidation:

- Personal Loan for Debt Consolidation

- Balance Transfer of Loans

- Loan Against Asset (Secured Loan)

Each method has its own structure, eligibility requirements, and impact on your financial health. Let’s explore them in detail.

1. Personal Loan for Debt Consolidation

This is the most popular and straightforward method of debt consolidation in India. It involves taking a new unsecured personal loan to repay all your existing loans. Once all other dues are cleared, you are left with a single EMI on the new loan.

How it works:

- You apply for a personal loan for the total amount of your existing debts.

- Once approved, you use the disbursed funds to pay off all existing loans.

- You then repay the new personal loan over a chosen tenure with fixed EMIs.

Suitable for:

- Borrowers with multiple unsecured loans

- Individuals with a good credit score (typically 700+)

- People who prefer a quick and digital application process

Pros:

- No need to pledge any collateral

- Fast disbursal (often within 24–48 hours)

- Fixed EMIs make monthly budgeting easier

- Helps improve credit score with disciplined repayments

Cons:

- Slightly higher interest rate compared to secured options

- Depends heavily on your credit score and income profile

RupeeQ Tip: You can check pre-approved personal loan offers for debt consolidation on RupeeQ in minutes. This saves time and helps you avoid unnecessary hard credit inquiries.

2. Balance Transfer of Loans

Balance transfer is a targeted consolidation method where you transfer one or more high-interest loans to a lender offering lower interest rates. Some banks also allow you to club multiple loans together during a balance transfer.

How it works:

- You approach a new lender with your existing loan details.

- The new lender pays off your current loan(s) directly to the old lender(s).

- You start repaying the new loan to the new lender at a lower interest rate.

Suitable for:

- Borrowers paying high interest on current loans

- Individuals with long repayment tenure left

- Salaried professionals looking for structured EMI reduction

Pros:

- Significant interest savings over time

- Option to choose new tenure or top-up loan amount

- Improves repayment flexibility

Cons:

- Some banks charge a processing fee or transfer fee

- Not suitable for small loans or if few EMIs are remaining

- May involve paperwork and re-verification of documents

Example:

If you have a personal loan of ₹3 lakh at 15% interest, and a bank offers a balance transfer at 11%, switching can reduce both EMI and total interest outgo.

RupeeQ Tip: Use RupeeQ’s comparison feature to evaluate balance transfer offers from different lenders and choose the one that provides actual savings after factoring in fees.

3. Loan Against Asset (Secured Loan for Consolidation)

This method involves using a personal asset—like a fixed deposit, gold, or property—as collateral to raise a loan. The funds are then used to pay off all existing debts. Since it’s a secured loan, the interest rates are usually lower than unsecured options.

How it works:

- You apply for a secured loan by pledging an asset.

- The lender disburses the amount after valuation and approval.

- You use the funds to repay outstanding loans.

- You repay the new loan as per agreed EMI schedule.

Suitable for:

- Individuals with moderate credit score but valuable assets

- Borrowers looking for lower interest rates

- People who need a larger loan amount or longer tenure

Pros:

- Lower interest rates due to collateral security

- Higher loan amount eligibility

- Flexible repayment terms

Cons:

- Risk of asset loss if you default

- Longer approval and documentation process

- Not ideal for small loan amounts

RupeeQ Tip: Go for a secured loan only if you are confident about repayment. Otherwise, an unsecured consolidation loan is safer and quicker.

Comparison Table: 3 Methods of Debt Consolidation

| Method | Type | Interest Rate | Collateral | Speed of Processing | Best For |

| Personal Loan | Unsecured | Moderate | No | Fast | Salaried individuals with good credit |

| Balance Transfer | Unsecured | Low (if eligible) | No | Moderate | High-interest loan holders |

| Loan Against Asset | Secured | Low | Yes | Slow | Asset owners with poor credit |

Choosing the Right Method of Consolidation

Each method has its own advantages, and the right option depends on your financial profile, credit score, loan amount, and comfort with collateral.

You should go for:

- Personal loan consolidation if you need fast processing and don’t want to risk any asset.

- Balance transfer if your primary concern is reducing interest rate on a large ongoing loan.

- Loan against asset if you have a secured asset and want a lower rate but don’t mind a longer process.

Final Thoughts

Debt consolidation is not a product—it’s a strategy. Whether you choose a personal loan, balance transfer, or a loan against property, the goal is the same: to simplify your finances and reduce the pressure of multiple EMIs.

By understanding the three major methods of consolidation and their suitability, you can choose the best option based on your personal situation. The key is to plan wisely, compare offers, and avoid overborrowing in the name of convenience.

Looking to consolidate your loans today?

Visit RupeeQ.com to check your credit score, explore personal loan offers, and compare consolidation options—all in one place. Simplify your repayments and make your money work smarter.