If you’re struggling to keep up with multiple EMIs each month, debt consolidation might seem like the perfect solution. But before making a decision, it’s important to understand exactly what happens when you consolidate your debts. How does it work? What changes in your financial life? And most importantly—does it actually help?

In this blog, we’ll walk you through what really happens after you consolidate your debts—step by step—along with the benefits, risks, and impact on your credit score and finances.

What Does It Mean to Consolidate Your Debts?

Debt consolidation means combining multiple existing loans—such as personal loans, education loans, or digital credit—into one new loan. Instead of paying several EMIs to different lenders, you pay one single EMI every month to a new lender.

The new loan amount is used to repay all your outstanding balances, and your new repayment begins with fresh terms: a new tenure, interest rate, and repayment plan.

What Happens Immediately After You Consolidate?

Once you consolidate your debt, several things happen in quick succession:

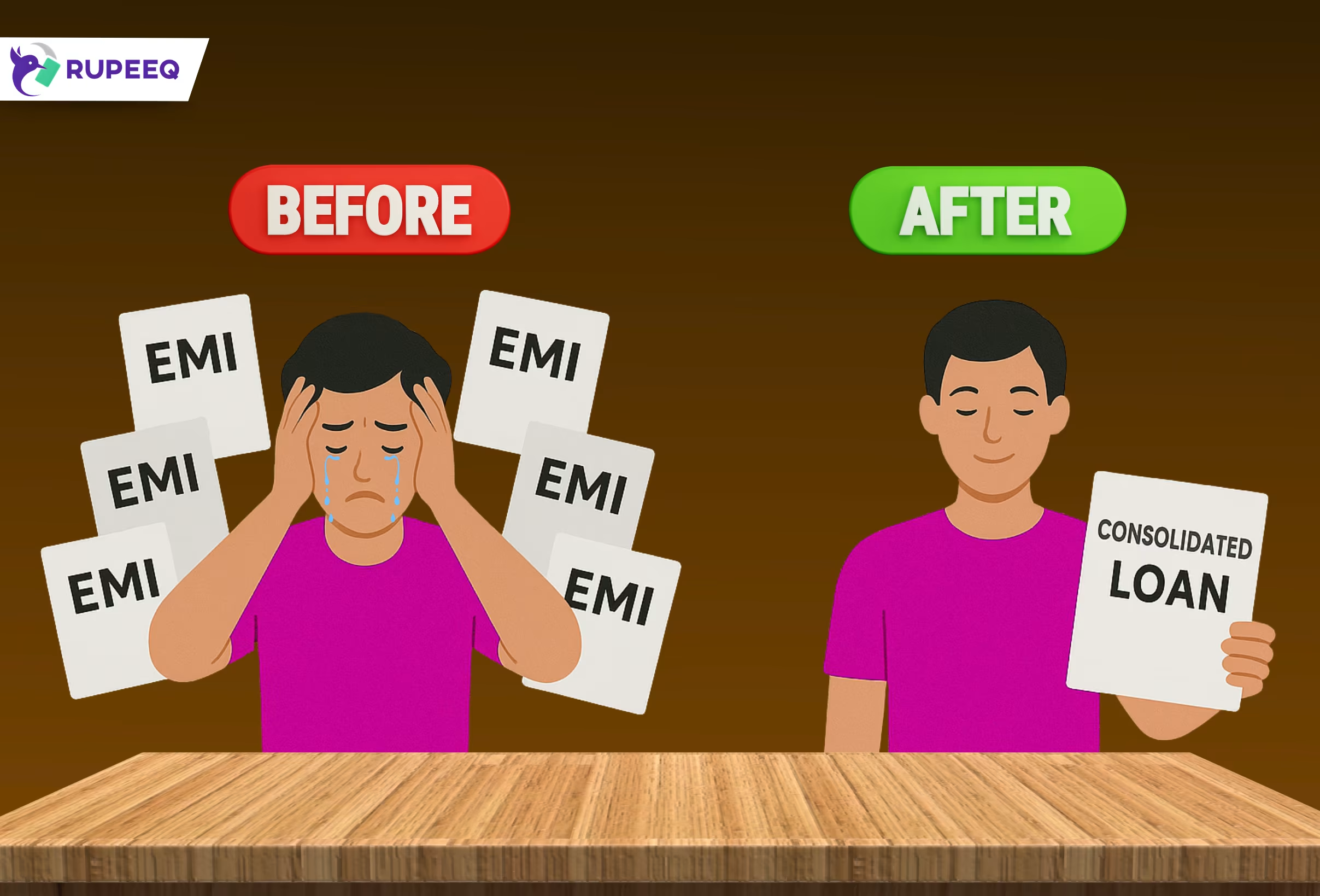

1. Your Old Loans Get Closed

The amount from your new loan is used to repay all your active loans. These accounts are marked “Closed” on your credit report.

Impact:

You are no longer liable to pay those old EMIs. You now have just one loan to manage, making your finances simpler and more transparent.

2. A New Loan Account Is Created

The new consolidated loan shows up as a fresh account on your credit report. It reflects the total amount borrowed, your EMI, interest rate, and tenure.

Impact:

There may be a temporary dip in your credit score due to a new credit inquiry and account opening, but this is normal and corrects over time.

3. You Start a New EMI Cycle

Your first EMI towards the new loan begins based on your selected repayment date. This new EMI replaces all your previous EMIs, which means you now have one fixed obligation to track every month.

Impact:

This greatly reduces the mental load of managing finances. You can set an auto-debit or reminder for one EMI instead of several.

RupeeQ Tip: Use the EMI calculator on RupeeQ to select a tenure and EMI that fits your monthly budget before you apply.

How Does Debt Consolidation Affect My Monthly Budget?

After consolidation, your monthly outgo can either increase, decrease, or stay the same—depending on how you structure your new loan.

If You Choose a Longer Tenure:

Your EMI may reduce, giving you breathing space in your budget, but you’ll pay more interest overall.

If You Choose a Shorter Tenure:

Your EMI may stay the same or increase slightly, but you’ll save significantly on interest and get debt-free sooner.

Example:

You were paying:

- Personal Loan A: ₹7,500

- Education Loan: ₹4,000

- Digital Loan: ₹3,000

Total: ₹14,500

After consolidation into one ₹5 lakh loan for 5 years at 11.5%:

- New EMI: ₹11,000

Savings: ₹3,500 per month

Does Consolidation Improve My Credit Score?

Yes—if managed properly.

Short-Term Impact:

- You may see a small dip in score due to a new credit enquiry and account.

- Multiple loan closures and one new loan may lower your average credit age.

Long-Term Impact:

- Easier repayment means lower risk of missed EMIs.

- Consistent EMI payments improve your credit history.

- Your credit score starts recovering and improving over 6–12 months.

RupeeQ Tip: Check credit score for free on RupeeQ before and after consolidation. Monitoring your score helps you stay on track.

What Changes in Your Financial Life After Consolidation?

Debt consolidation doesn’t just change your loan—it changes your entire repayment strategy. Here’s what improves:

1. Simplified Finances

No more juggling due dates. One EMI, one date, one lender.

2. Better Financial Planning

A single EMI makes monthly budgeting easier and more predictable.

3. Reduced Risk of EMI Defaults

With only one EMI to remember, you reduce the risk of delays and bounce charges.

4. More Savings Opportunity

Lower EMIs = more monthly surplus = higher potential for savings or investing.

What Are the Benefits of Consolidating Your Debts?

| Benefit | Description |

| One EMI | Simplifies repayment |

| Better Rates | Replace high-interest loans with a cheaper one |

| Improved Credit | Timely payment on one loan builds your credit score |

| Lower EMI | Reduce monthly burden with a longer tenure |

| Mental Peace | Less stress, better control over finances |

Are There Any Risks After Consolidation?

Yes, there are a few risks you should be aware of:

1. Longer Tenure = More Interest

If you choose a very long tenure just to reduce EMI, you may end up paying more interest over time.

2. Overborrowing Temptation

Some borrowers take a higher loan than required during consolidation and use the extra money for spending. This creates unnecessary new debt.

3. New Defaults Can Hurt More

Now that your debt is consolidated, defaulting on this single loan can significantly hurt your credit profile.

What Should You Do After Consolidating?

Consolidating debt is only step one. Here’s what you should do after:

- Stick to your EMI schedule without fail

- Avoid taking fresh loans unless absolutely necessary

- Use the savings in your monthly budget to build an emergency fund

- Track your credit score monthly

- Try to prepay or foreclose the loan early if possible

RupeeQ Tip: Choose lenders that allow part-prepayment without penalty. RupeeQ highlights these details during your offer comparison.

So, what happens when you consolidate your debts?

You close your old loans, start repaying a new one, simplify your monthly finances, and—if you’re disciplined—set yourself up for long-term credit health.

Debt consolidation isn’t a shortcut. It’s a strategy to organise your repayment better and save on cost and confusion. But it works best when paired with responsible borrowing habits.

Ready to simplify your loans?

Visit RupeeQ.com to check your credit score, compare debt consolidation offers, and take your first step toward financial freedom—with just one EMI.