Debt can be empowering when managed well—but overwhelming when it starts affecting your savings, lifestyle, or peace of mind. Whether you’re handling personal loans, credit card dues, or digital credit lines, the key to becoming debt-free lies in choosing the right repayment strategy. In this blog, we’ll walk you through the best ways to pay off debt in India, supported by practical steps, smart tools, and RupeeQ tips to help you get started.

Why You Need a Debt Repayment Strategy

If you’re repaying more than one loan or EMI, having a strategy is essential. Without it, you may:

- End up paying more interest than needed

- Miss due dates and damage your credit score

- Feel financially stretched every month

- Fall into a cycle of borrowing to repay other loans

By choosing the right approach, you can regain control over your income, improve your credit score, and start saving again.

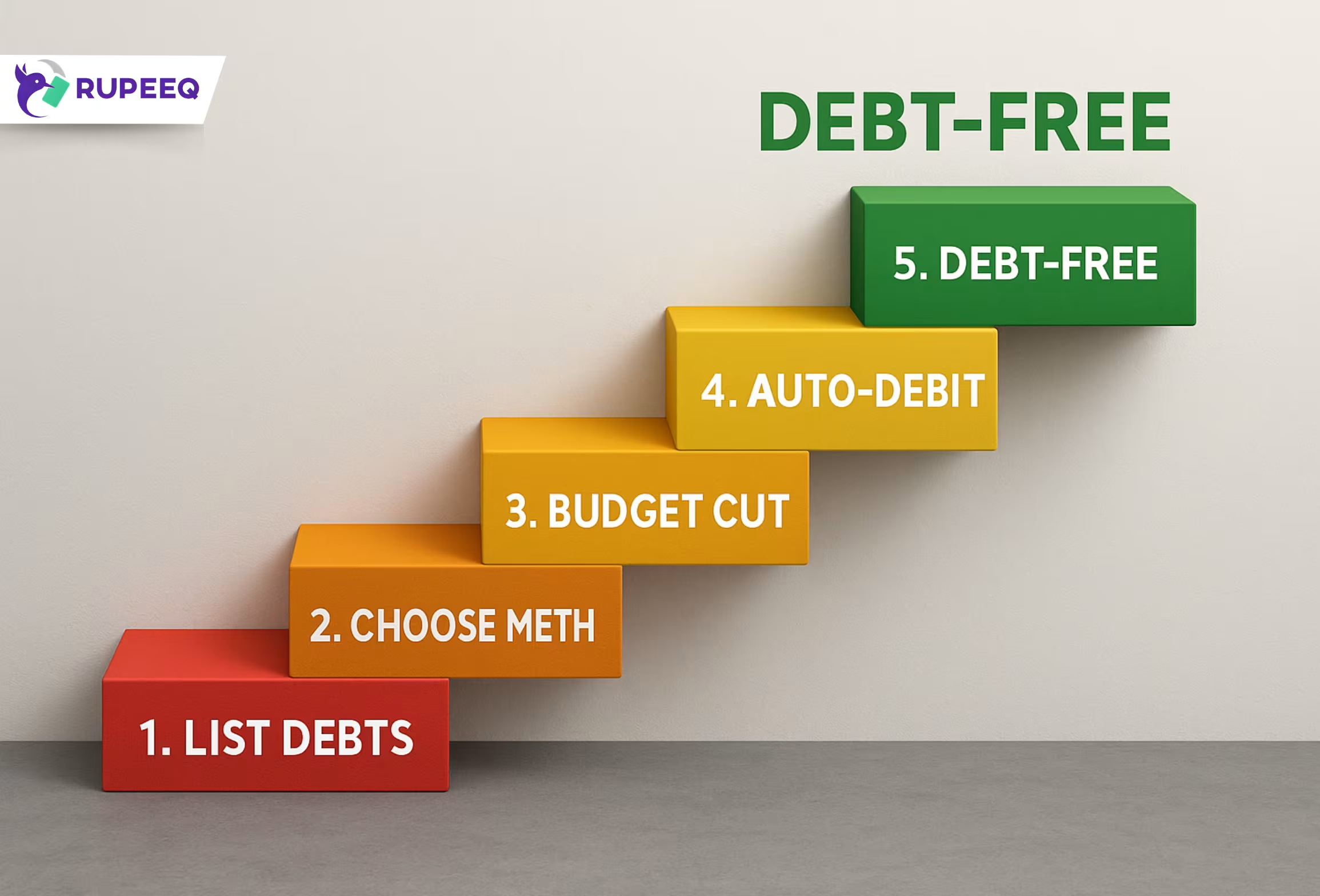

1. Create a Complete Debt List

Before you begin repayment planning, take stock of your current debts.

Write down for each loan or credit:

- Total outstanding amount

- Interest rate

- Monthly EMI

- Tenure remaining

- Due date

- Lender name

This gives you a clear picture of your liabilities.

RupeeQ Tip: If you’re unsure about your current debt position, check free credit report on RupeeQ. It will list all active loan accounts and credit utilization.

2. Prioritize High-Interest Debt First (Avalanche Method)

The avalanche method is one of the most efficient ways to repay debt. You continue paying the minimum on all loans but use any extra funds to repay the highest-interest debt first.

Why it works:

- You reduce the most expensive debt first

- Saves the most on total interest paid

Suitable for:

- People with stable monthly income

- Borrowers who can resist the urge to close small loans first

Example:

If you have a credit card at 36% and a personal loan at 14%, focus on repaying the credit card first while continuing minimum payments on other EMIs.

3. Pay Off Small Balances First (Snowball Method)

If motivation and momentum matter more to you, the snowball method might work better. Here, you repay the smallest outstanding loans first, while making minimum payments on larger ones.

Why it works:

- Gives quick wins and builds repayment discipline

- Reduces the number of active loans early on

Suitable for:

- People who feel overwhelmed by multiple loan accounts

- Those who need psychological motivation to stay on track

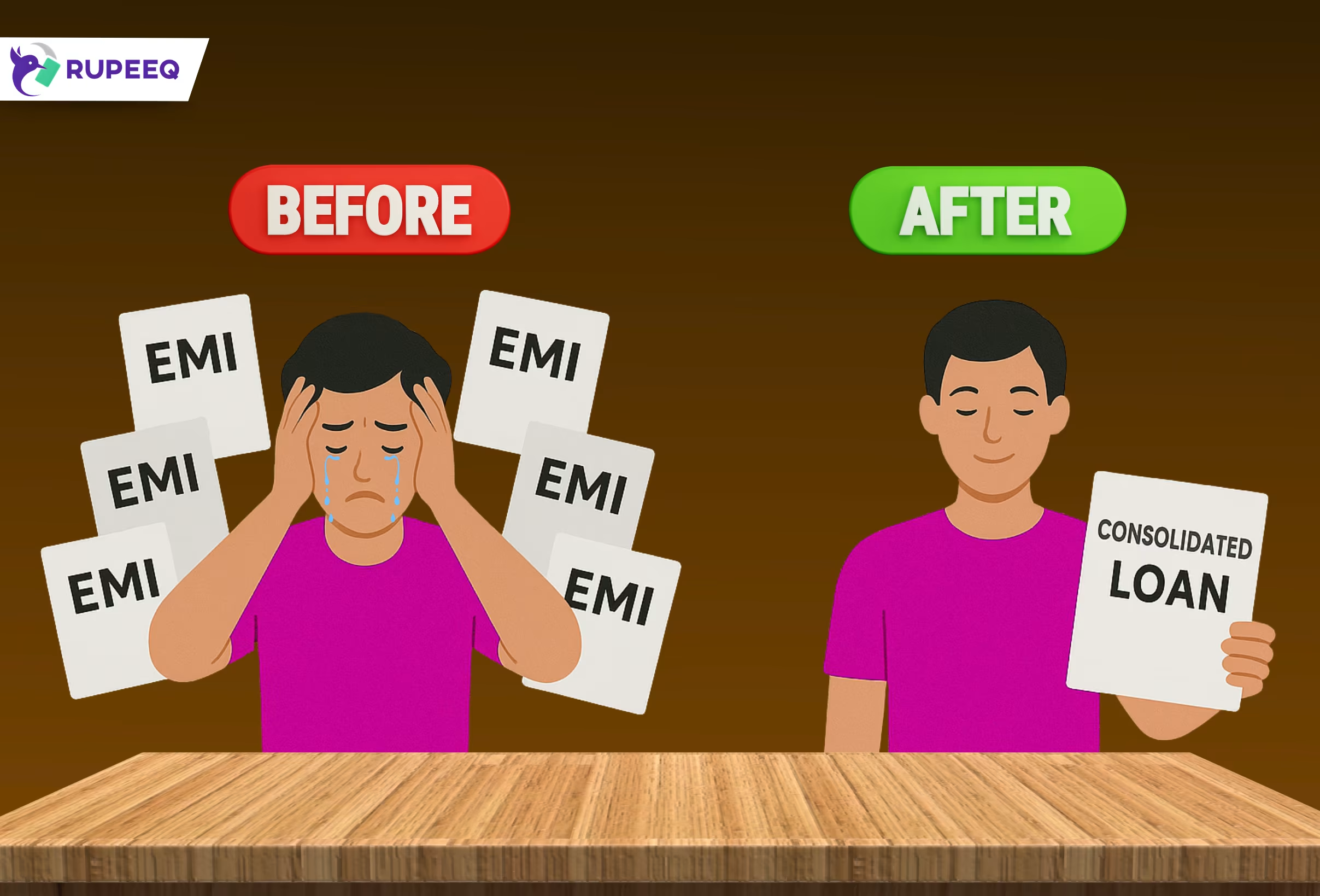

4. Consolidate Your Debts into One Loan

If you’re dealing with multiple high-interest loans or EMIs, the best way to simplify your finances may be through debt consolidation.

What is debt consolidation?

It means taking a new personal loan to repay all your existing loans. You then repay just one EMI each month at a potentially lower interest rate.

Benefits:

- One EMI, one due date

- Lower interest cost if you qualify for a better rate

- Easier to manage and track

RupeeQ Tip: Use RupeeQ to check if you’re eligible for a debt consolidation loan with lower interest. You can compare pre-approved offers instantly.

5. Use Windfalls or Bonuses Wisely

Got a tax refund, performance bonus, or incentive payout? Instead of spending it all, use a portion to make a lump sum repayment toward your highest-interest loan.

Even a one-time prepayment can reduce:

- Interest burden

- EMI amount (if tenure is unchanged)

- Loan tenure (if EMI remains the same)

Note: Check if your lender allows part-prepayments without penalty.

6. Set Up Auto-Debits and Reminders

Even with the right strategy, missing a payment can hurt your credit score. Set up auto-debit mandates or reminders so you never miss a due date.

Why it matters:

- Avoids penalties and late fees

- Maintains repayment discipline

- Builds a positive credit history

7. Cut Down Non-Essential Expenses

To pay off debt faster, create a budget and look for areas where you can save. These savings can then be directed toward debt repayment.

Smart ways to cut costs:

- Cancel unused subscriptions

- Reduce eating out or online shopping

- Shift to a more affordable mobile/data plan

- Reassess insurance premiums or EMI protection plans

RupeeQ Tip: Even saving ₹2,000/month and directing it toward a 14% personal loan can reduce your overall interest cost significantly.

8. Don’t Take New Loans While Repaying Old Ones

This is where many borrowers go wrong—taking fresh credit while still repaying existing loans. It increases your debt burden and can stretch your finances thin.

Why to avoid:

- Higher debt-to-income (DTI) ratio

- May impact your credit score

- Increases chances of default

Stick to the goal: Repay what you owe before borrowing again.

9. Track Your Progress Regularly

Keep checking how your repayments are affecting your:

- Outstanding principal

- Credit score

- EMI schedule

Celebrate small milestones like closing a loan account or improving your credit score by 20–30 points.

RupeeQ Tip: You can track your credit improvement journey on RupeeQ by checking your free score every month.

10. Seek Help if You’re Struggling

If you’re unable to keep up with repayments:

- Contact your lender and request a restructuring

- Ask for an EMI pause or tenure extension

- Explore secured loan options for lower rates

Avoid loan apps or informal credit sources, as they often charge high interest and have poor customer practices.

Summary Table: Best Ways to Pay Off Debt

| Strategy | Best For | Key Benefit |

| Avalanche Method | Financially disciplined borrowers | Saves most interest |

| Snowball Method | Those needing motivation | Faster sense of progress |

| Debt Consolidation | Borrowers with multiple EMIs | One EMI, lower cost |

| Lump Sum Repayment | Bonus/incentive earners | Cuts EMI or tenure |

| Budget Cuts | High-expense lifestyles | More funds for debt |

| Auto-Debits | Everyone | Avoid missed payments |

Final Thoughts

The best way to pay off debt depends on your financial behavior, current liabilities, and income flow. Whether it’s following the avalanche method, consolidating debt, or using bonuses wisely—the goal remains the same: become debt-free without compromising your financial stability.

Start with awareness, follow it with action, and stay consistent.

Want to simplify your repayments?

Use RupeeQ.com to check your credit score, consolidate your loans smartly, and get back on the path to financial freedom.