When facing a financial need, whether it’s an emergency, home renovation, wedding expenses, or debt consolidation, two common borrowing options are personal loans and credit cards. Both provide access to funds without requiring collateral, but they differ significantly in terms of repayment structure, interest rates, and ideal usage.

A personal loan is best suited for larger, planned expenses that require structured repayment over time, while a credit card is better for short-term spending and managing everyday expenses. Knowing when to choose one over the other can help you avoid high-interest costs and financial strain.

This blog explains when a personal loan is a better option than a credit card, along with insights on choosing the right borrowing method for different financial situations.

When You Need a Large Loan Amount

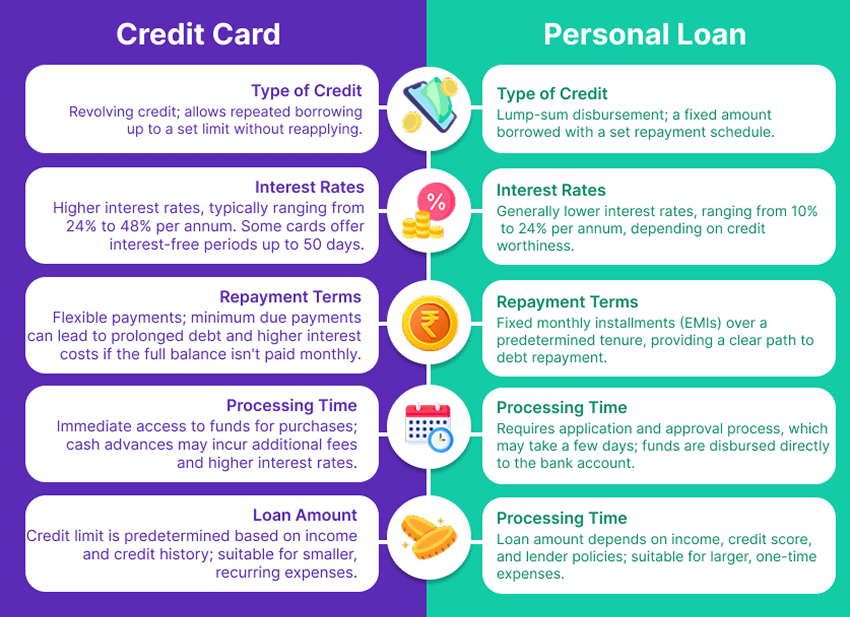

A personal loan is the preferred choice when you need to borrow a large sum of money. Credit cards come with a pre-approved credit limit, which may not be sufficient for high-value expenses.

Why Choose a Personal Loan?

- Personal loans offer higher loan amounts, ranging from ₹50,000 to ₹50 lakh, depending on your eligibility.

- Credit cards, on the other hand, typically have a spending limit of ₹10,000 to ₹10 lakh, which may not be enough for major expenses.

- Repayment in structured EMIs makes personal loans easier to manage for larger amounts.

When to Use a Credit Card Instead?

- For small purchases like shopping, dining, or short-term expenses that can be repaid within the interest-free period.

RupeeQ Tip – If your financial need exceeds your credit card limit, opting for a personal loan ensures adequate funds without maxing out your card.

When You Need Lower Interest Rates

Interest rates are a major factor when deciding between a personal loan and a credit card. Personal loans generally come with lower interest rates compared to credit cards, making them more cost-effective for long-term borrowing.

Why Choose a Personal Loan?

- Personal loans typically have interest rates ranging from 10% to 24% per annum.

- Credit cards have significantly higher rates, usually between 24% and 48% per annum if you carry a balance.

- For longer repayment periods, a personal loan saves money compared to rolling over credit card debt.

When to Use a Credit Card Instead?

- If you can pay the full credit card balance before the due date, avoiding interest completely.

RupeeQ Tip – If you are considering converting a credit card balance into EMIs, check the interest rate. It may be higher than a personal loan, making a loan a smarter choice.

When You Need Fixed EMIs for Easy Repayment

A personal loan follows a structured repayment plan, where the EMI remains the same throughout the loan tenure. This predictability makes budgeting easier compared to credit card payments, which can vary based on spending.

Why Choose a Personal Loan?

- Personal loans come with fixed EMIs, allowing you to plan your monthly budget efficiently.

- Credit cards require at least a minimum payment each month, but unpaid balances accumulate high-interest charges.

- Personal loans offer repayment tenures ranging from 12 months to 7 years, giving flexibility in managing finances.

When to Use a Credit Card Instead?

- If you need short-term credit and are confident you can repay the full amount within the next billing cycle.

RupeeQ Tip – A personal loan is ideal for salaried and self-employed individuals who prefer structured EMIs over fluctuating credit card dues.

When You Need Funds for Debt Consolidation

If you are struggling with multiple debts—such as credit card balances, personal loans, or other high-interest borrowings—a personal loan can help consolidate them into a single lower-interest EMI.

Why Choose a Personal Loan?

- Consolidating debts into a personal loan at a lower interest rate reduces your overall repayment burden.

- Personal loans simplify repayments by replacing multiple debts with a single EMI, making it easier to track.

- Paying off high-interest credit card debt with a lower-interest personal loan saves money.

When to Use a Credit Card Instead?

- If you have a low outstanding balance on your credit card and can clear it in the next cycle.

RupeeQ Tip – If you have multiple credit card debts, a personal loan for debt consolidation can provide financial relief and improve your credit score.

When You Need a Longer Repayment Period

Credit cards require you to repay the full balance every month to avoid high-interest charges. If you need a longer repayment period, a personal loan is a better option.

Why Choose a Personal Loan?

- Personal loans offer tenures ranging from 12 months to 7 years, allowing you to spread repayments over time.

- Credit cards only provide a 30-50 day interest-free period, after which high-interest charges apply.

- A longer tenure reduces monthly EMI burden, making large expenses more manageable.

When to Use a Credit Card Instead?

- If you don’t need an extended repayment period and can clear the dues quickly.

RupeeQ Tip – If you need more than 6 months to repay a borrowed amount, a personal loan is the more cost-effective choice.

When You Need Emergency Funds Without a Credit Card Limit

If you don’t have a high credit card limit, a personal loan can be a better alternative for emergencies. Many lenders now offer instant personal loans with quick disbursals, making them a viable option for urgent financial needs.

Why Choose a Personal Loan?

- Personal loans are available even if your credit card limit is low or already used up.

- Many lenders offer instant approval and disbursal within 24 hours, making it ideal for emergencies.

- Credit card cash withdrawals attract high-interest rates and cash advance fees, making personal loans a cheaper option.

When to Use a Credit Card Instead?

- If the emergency expense is small and you can repay it in full within the interest-free period.

RupeeQ Tip – If you need funds beyond your credit card limit, a personal loan provides quick access at a lower cost.

When to Choose a Personal Loan Over a Credit Card

A personal loan is the right choice when you need a large loan amount, lower interest rates, structured EMIs, and longer repayment tenure. On the other hand, a credit card is better for short-term spending and transactions that can be cleared within the interest-free period.

Key Takeaways:

- Choose a personal loan for large expenses, structured EMIs, and lower interest rates.

- Use a credit card for short-term needs that can be repaid quickly.

- If you are carrying high credit card balances, consolidating them with a personal loan can reduce financial strain.

- Personal loans provide higher borrowing limits and longer tenures, making them suitable for planned expenses.

- If you are in an emergency and don’t have a high credit card limit, a personal loan is a reliable alternative.

If you are unsure which option is best for you, compare personal loan offers on RupeeQ and choose the most cost-effective borrowing method today.