When you’re dealing with financial obligations, both personal loans and debt consolidation loans can seem like attractive options. But which one is better? Should you take a regular personal loan, or is debt consolidation the smarter move if you’re already juggling multiple loans?

In this blog, we’ll explain the difference between a personal loan and a debt consolidation loan, their pros and cons, and when one is better than the other. By the end, you’ll be able to decide which option best suits your financial goals.

Understanding the Basics

Before comparing, let’s define each term clearly.

What is a Personal Loan?

A personal loan is an unsecured loan you can take for various reasons—wedding, travel, education, medical expenses, or even managing existing debts. The lender disburses the entire amount upfront, and you repay it in fixed EMIs over a chosen tenure.

What is a Debt Consolidation Loan?

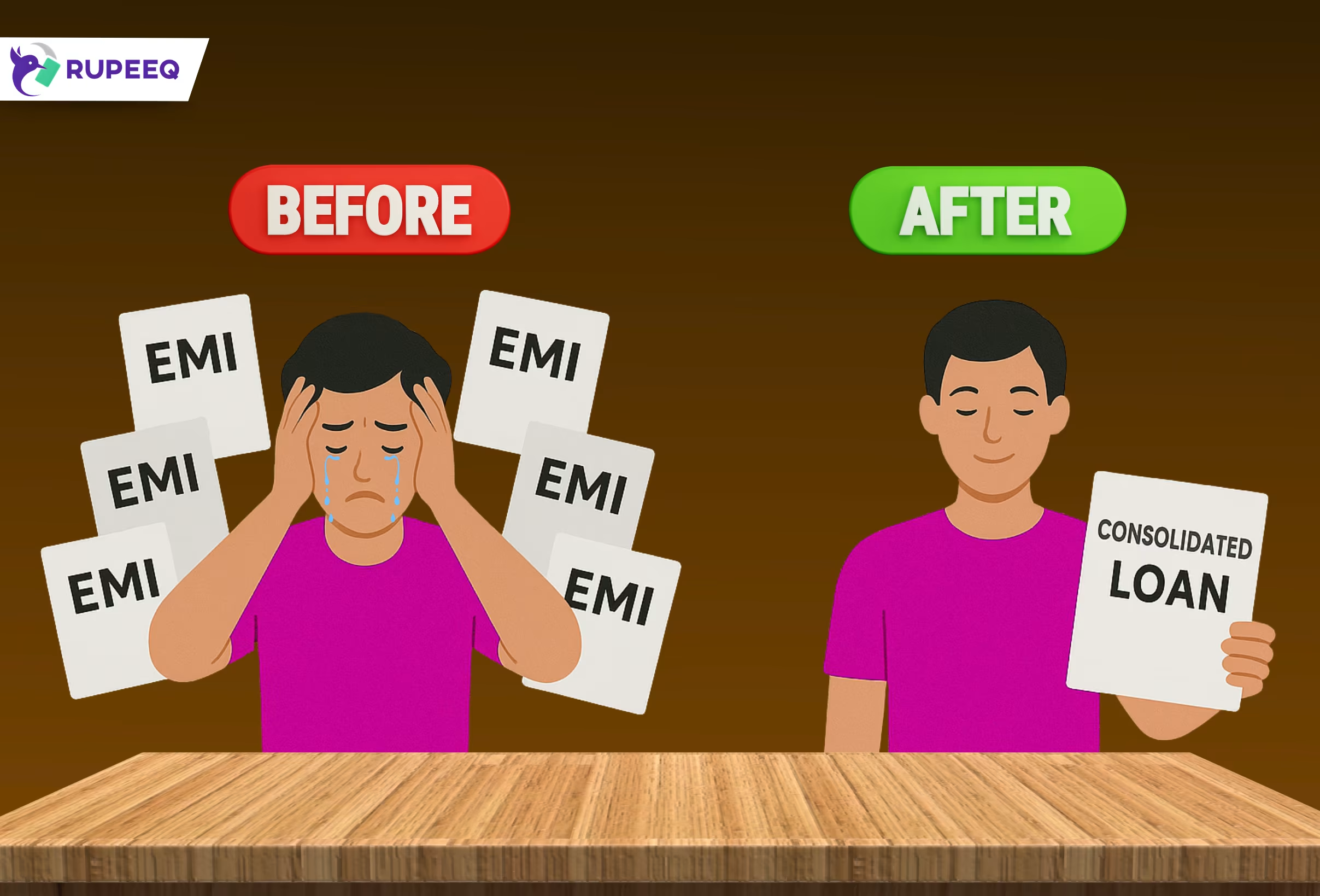

A debt consolidation loan is a type of personal loan specifically used to combine multiple existing loans into one. Instead of paying several EMIs each month, you repay just one loan with a single EMI. It’s designed to simplify repayment and often reduce your total interest outgo.

RupeeQ Tip: Debt consolidation loans are available on RupeeQ as part of personal loan offers, tailored based on your credit profile and current liabilities.

Key Differences Between Personal Loan and Debt Consolidation

| Feature | Personal Loan | Debt Consolidation Loan |

| Purpose | Can be used for any financial need | Specifically to pay off existing loans |

| EMI Count | Adds a new EMI to your current liabilities | Replaces multiple EMIs with one |

| Credit Score Use | Based on income and score | Score + current loans evaluated |

| Interest Rate | Varies by profile and lender | Often lower if used to replace high-cost loans |

| Financial Benefit | Funds your needs | Restructures and simplifies debt |

| Credit Score Impact | Can hurt if used irresponsibly | Can improve if repaid on time |

When Should You Choose a Personal Loan?

A personal loan is suitable when you’re taking on a new expense rather than managing old debt.

Scenarios where personal loan is better:

- Medical emergencies or sudden financial gaps

- Big-ticket purchases like electronics or furniture

- Funding a wedding, trip, or home renovation

- You have no existing loans or only one active loan

Pros:

- Quick disbursal for urgent needs

- Flexible usage—no restriction on how the money is spent

- Tenure and EMI can be chosen as per your budget

Cons:

- Adds to your existing EMI load

- Higher chance of default if taken without planning

When Should You Choose a Debt Consolidation Loan?

Debt consolidation is ideal when you’re struggling to manage multiple EMIs or want to reduce the interest burden on current loans.

Scenarios where debt consolidation is better:

- You have 2 or more ongoing personal loans or credit lines

- Your total EMI outgo is affecting monthly cash flow

- You want to reduce chances of missed payments

- You want to improve your credit score through consistent EMI tracking

Pros:

- One EMI instead of many

- Lower interest cost if replacing high-interest loans

- Improved credit score with regular repayment

- Helps avoid late payment penalties

Cons:

- Can backfire if you borrow more than you need

- A temporary dip in credit score due to account changes

Example Comparison

Let’s say you have:

- Loan A: ₹2 lakh at 14% (EMI: ₹6,800)

- Loan B: ₹1.5 lakh at 16% (EMI: ₹5,200)

- Loan C: ₹1 lakh at 18% (EMI: ₹3,600)

Total EMI: ₹15,600

Now you take a debt consolidation loan of ₹4.5 lakh at 11.5% for 5 years:

New EMI: ₹9,900

Result:

- Savings of ₹5,700/month

- One EMI instead of three

- Lower overall interest outgo

RupeeQ Tip: Always compare your total cost of borrowing before and after consolidation. RupeeQ EMI calculator helps simulate this easily.

Credit Score Impact: Personal Loan vs Debt Consolidation

Personal Loan:

- Helps build credit if repaid on time

- Adds to your overall debt burden

- May reduce your score if your DTI (debt-to-income ratio) rises too high

Debt Consolidation Loan:

- May cause a small dip initially due to new loan enquiry

- But improves your score over time with disciplined repayment

- Shows financial responsibility to lenders

Which Loan is Better for Financial Discipline?

If your goal is to reduce debt and become financially stable, debt consolidation is the better choice. It helps you:

- Focus on one EMI

- Close old loan accounts

- Avoid default cycles

- Create a clear debt-free roadmap

If your goal is to meet a specific expense and you can comfortably handle additional EMIs, a personal loan works fine.

How RupeeQ Helps You Decide

RupeeQ makes it easy to compare personal loan and debt consolidation options in one place. You can:

- Check your credit score

- See eligible offers instantly

- Use EMI calculator for different tenures

- Compare lender-wise interest rates and terms

- Apply online without affecting your credit score

RupeeQ Tip: Always start by checking your credit score for free on RupeeQ. It helps you understand which type of loan you’re more likely to get approved for at better terms.

Final Thoughts

So, which is better: a personal loan or debt consolidation?

- If you need funds for a specific goal or emergency, and you don’t already have heavy loan obligations, a personal loan is the better option.

- If you’re overwhelmed by multiple EMIs and want to simplify your financial life while potentially reducing interest cost, debt consolidation is the smarter choice.

The decision depends on your financial situation, income stability, credit score, and ability to manage repayments.

Looking to make the right loan move?

Check your credit score, explore both personal loan and debt consolidation offers, and choose what’s best for you—only on RupeeQ.com. One platform, smarter choices.