Your car breaks down, a medical bill shows up, or your landlord demands two months’ rent overnight. These situations don’t wait for your next salary credit. And if your savings aren’t enough to cover it, you need money fast.

That’s exactly where emergency loan options in India come in. But not all of them work the same way, and picking the wrong one can leave you paying far more than you needed to.

Here’s a practical breakdown of what’s available right now and how to choose what fits your situation.

What Counts as an Emergency Loan?

An emergency loan is any short-term borrowing you take to handle an urgent, unplanned expense. It’s not a home loan or a car loan. The need is immediate, and the disbursement has to match that urgency.

In India, emergency loans typically fall under:

- Personal Loans from banks or NBFCs

- Salary advance loans

- Gold loans

- Loans against fixed deposits or insurance policies

- Credit Card EMI conversions or cash advances

- Flexi loans and Overdraft facilities

Each option has different eligibility requirements, turnaround times, and costs.

Best Emergency Loan Options in India

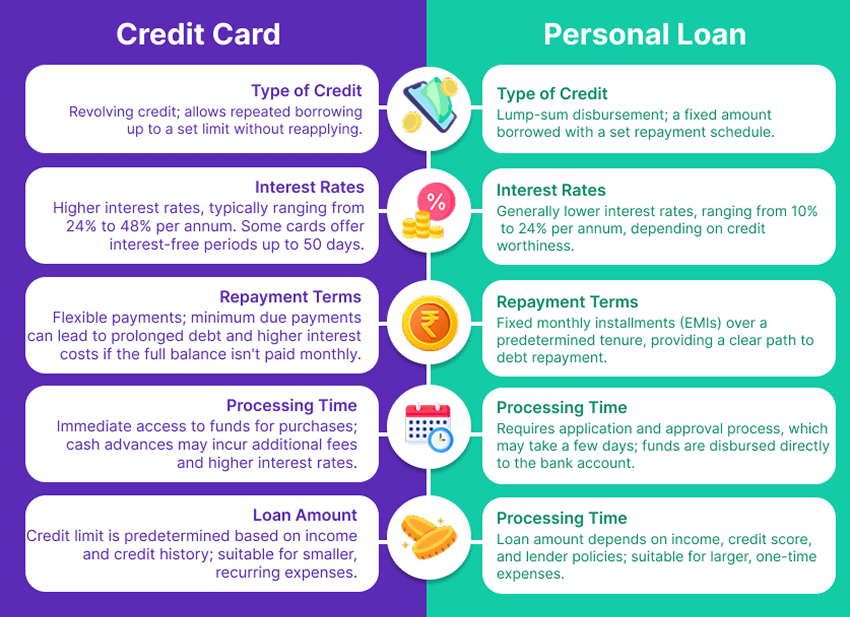

1. Personal Loans from NBFCs and Banks

This is the most commonly used emergency loan option in India. Fully unsecured, no collateral needed, and disbursed quickly once documents are verified.

Key things to know:

- Loan amounts typically range from ₹50,000 to ₹5 lakh

- Tenure options run from 12 to 60 months

- Interest rates range from 10.5% to 36% per year, depending on your credit profile

- Top NBFCs like Bajaj Finserv, Tata Capital, and Poonawalla Fincorp offer same-day or next-day disbursal

Your credit score plays a big role here. According to HDFC bank, borrowers with a score of 750 and above are significantly more likely to get approved at competitive rates.

Who it works best for: Salaried individuals with a steady income and a decent credit score who need ₹50,000 or more urgently.

RupeeQ Tip: Before applying for a Personal Loan, check your free credit score on RupeeQ ACE. It gives you a clear picture of where you stand and which lenders are likely to approve you without wasting a hard inquiry.

2. Flexi Loans and Overdraft Facilities

This is one of the most underused emergency loan options in India, and often the smartest one if you qualify.

A Flexi Loan or Overdraft works like a credit line. The lender approves a limit upfront. You draw only what you need, when you need it, and pay interest only on the amount used, not the full limit. However, it is crucial to avoid over-borrowing with a flexi loan.

How it works:

- You get a pre-approved limit, say ₹2 lakh

- You withdraw ₹40,000 for the emergency

- Interest is charged only on ₹40,000, not ₹2 lakh

- Repay and withdraw again within the tenure without reapplying

Several banks offer Overdraft facilities linked to salary accounts or FDs.

Key details:

- Interest rates are similar to Personal Loans, typically 11% to 30% per year

- Processing is done once upfront; no fresh application for each withdrawal

- Some lenders charge a small fee on the unused limit

Who it works best for: Borrowers who aren’t sure of the exact amount needed upfront, or those who face recurring short-term cash gaps.

3. Credit Card EMI Conversion or Cash Advance

If you have a Credit Card with an available limit, two options exist.

- EMI conversion: Convert a large upcoming expense directly to EMIs at a pre-agreed interest rate, often between 12% and 18% per year. This works well for planned emergency purchases like a hospital procedure or appliance replacement.

- Cash advance: Withdraw cash directly from your Credit Card at an ATM. This is fast but expensive. Interest starts from day one, with no grace period, and rates can go up to 36% to 42% annually.

Use EMI conversion when you can. Avoid cash advances unless there’s no other option.

Who it works best for: Existing Credit Cardholders who need speed and already have a limit available.

RupeeQ Tip: Use RupeeQ’s free EMI Calculator to compare the total interest cost of a Credit Card EMI versus a standard term loan before you decide. The difference can be significant if you’re likely to repay early.

4. Salary Advance Loans

If you’re salaried, your employer or a lender can advance a portion of your upcoming salary as a loan. Some companies offer this in-house through HR. Others connect employees with platforms like EarlySalary (now Fibe) or KreditBee.

How it works:

- You get a portion of next month’s salary credited upfront

- The amount is deducted automatically on your next payday

- Interest is charged only for the days you hold the money

This is one of the fastest emergency loan options in India, often disbursed within hours.

Who it works best for: Salaried employees who need a small, short-term bridge of ₹5,000 to ₹1 lakh and can repay within 30 to 90 days.

5. Gold Loans

If you have gold jewelry or coins at home, a gold loan is one of the most accessible emergency options, regardless of your credit score.

What makes it practical:

- No credit score requirement

- Approval and disbursal often happens the same day, sometimes within 30 minutes

- Lenders like Muthoot Finance and Manappuram are available across thousands of locations in India

- Interest rates are lower than unsecured Personal Loans, typically 9% to 24% per year

- You get up to 75% of the gold’s market value as a loan

Who it works best for: Anyone with idle gold who needs quick funds but has a low credit score or irregular income.

6. Loan Against Fixed Deposit (FD)

If you have an FD with a bank, you can take a loan against it without breaking it. You keep earning interest on the FD while borrowing against its value.

Key details:

- Borrow up to 85% to 95% of your FD value

- Interest charged is typically 1% to 2% above the FD rate

- No credit check needed

- Processed within one to two working days by most banks

This is one of the cheapest emergency loan options available if you have the asset.

Who it works best for: People with existing FDs who want low-cost credit without disturbing their savings.

How to Choose the Right Emergency Loan Option

With several options in front of you, the decision comes down to three things.

- How fast do you need the money?

Gold loans and fintech apps are fastest, often same-day. FD loans take a day or two. Personal Loans from banks can take two to five days.

- What’s your credit profile?

Strong credit score? Go for a Personal Loan or flexi loan at a competitive rate. Low or no credit score? Gold loans and FD loans are your better bet. If your score needs work before you apply, here are 6 easy steps to fix a bad credit score that can improve your chances quickly.

- How much do you need?

For under ₹50,000, salary advance or fintech apps make more sense. For larger amounts or recurring needs, Personal Loans, flexi loans, or gold loans work better.

What to Avoid During a Financial Emergency

A few common mistakes can make the situation worse:

- Applying to multiple lenders at once. Each application triggers a hard inquiry and lowers your credit score.

- Borrowing more than you need. Larger loans mean more interest, even if you’re approved for more.

- Ignoring prepayment terms. Some lenders charge prepayment fees. Check before signing.

- Taking a cash advance on a Credit Card when cheaper options are available.

To avoid these mistakes, visit RupeeQ.com and compare all the available loan offers at one place, before applying anywhere else.

Quick Comparison Table

| Loan Type | Speed | Credit Score Needed | Best For |

| Personal Loan (NBFC) | Same to next day | 700+ preferred | Larger amounts, salaried |

| Flexi Loan / Overdraft | Same to next day | 700+ preferred | Uncertain amounts, recurring gaps |

| Salary Advance | Same day | Not required | Small short-term needs |

| Gold Loan | Same day | Not required | Quick funds, any profile |

| FD Loan | 1-2 days | Not required | Low-cost credit with FD |

| Credit Card EMI | Instant | Existing card needed | Planned emergencies |

Final Thought

A financial emergency rarely gives you time to research. Knowing your options before the need arises puts you in a better position to act quickly without making an expensive mistake.

The best emergency loan option in India is the one that fits your credit profile, asset situation, and the exact amount you need. Start from those three points and the right choice becomes much clearer.

FAQs

-

Can I get an emergency loan in India with a low credit score?

Yes. Gold loans and FD loans don’t require a credit check. Some fintech platforms also work with borrowers who have limited or low credit histories. You can also read our dedicated guide on getting a Personal Loan with a low credit score for more options.

-

How fast can I get an emergency loan in India?

Gold loans and app-based lenders can disburse within a few hours. Personal Loans from NBFCs typically disburse the same day or next day if documents are in order.

-

What is the minimum salary required for a Personal Loan?

Most banks require ₹25,000 per month. Several NBFCs approve loans for borrowers earning ₹12,000 to ₹15,000 per month.

-

What is the difference between a flexi loan and a regular Personal Loan?

A regular Personal Loan gives you the full amount upfront and charges interest on the entire principal from day one. A flexi loan gives you a credit limit you draw from as needed, with interest charged only on what you’ve actually used.

-

Is a gold loan better than a Personal Loan in an emergency?

If you have gold available, a gold loan is faster, cheaper, and doesn’t require a credit score. The downside is you need to pledge a physical asset.

-

Can self-employed individuals get emergency loans in India?

Yes, through gold loans, FD loans, and select NBFCs and fintech platforms that evaluate bank statements instead of salary slips.